To say UPS is a mess would be an understatement.

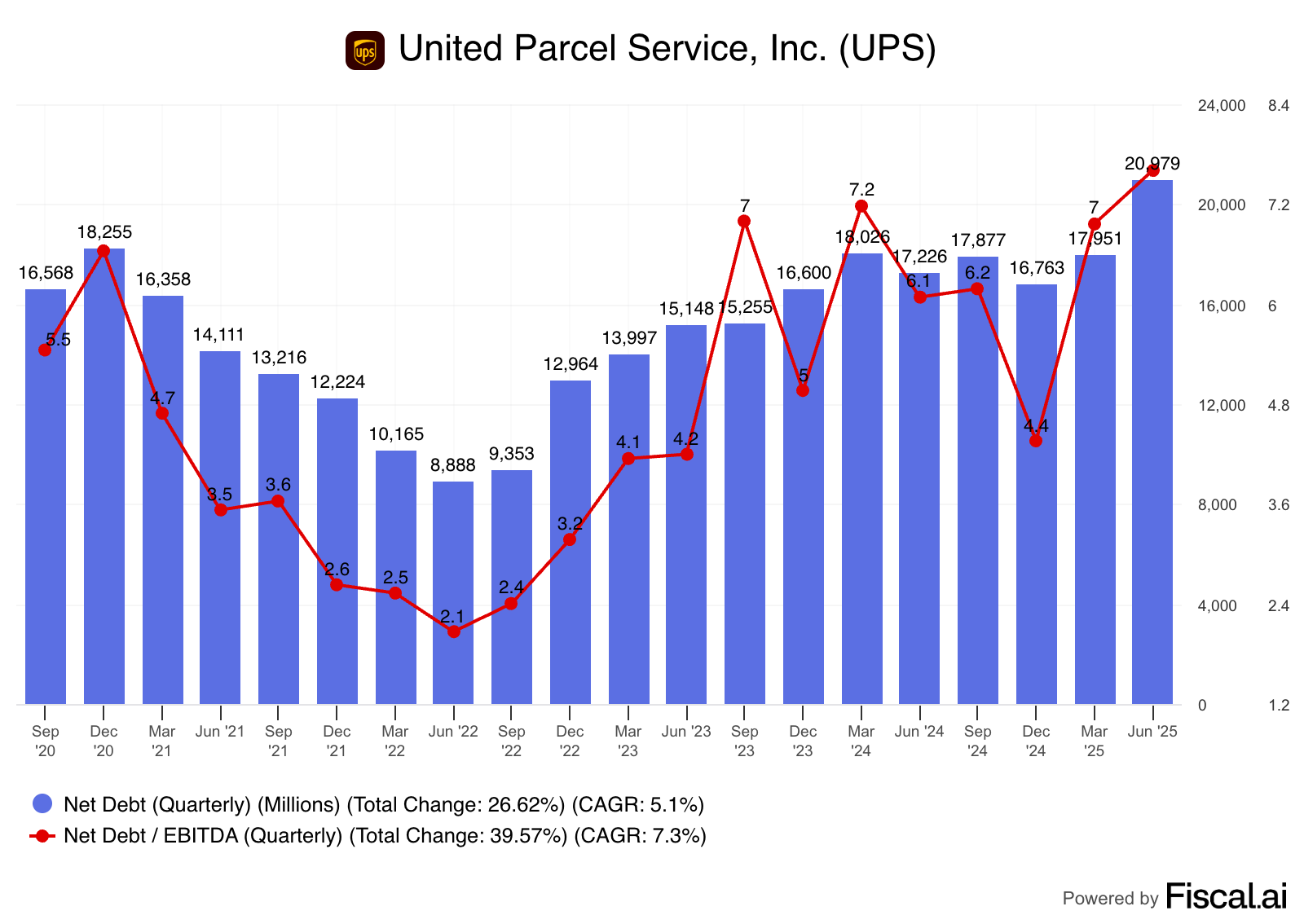

As is often the case, the story can best be told by a few charts, such as this one, which shows the rise in net debt...

Source: Fiscal AI (Click here for a full UPS overview)

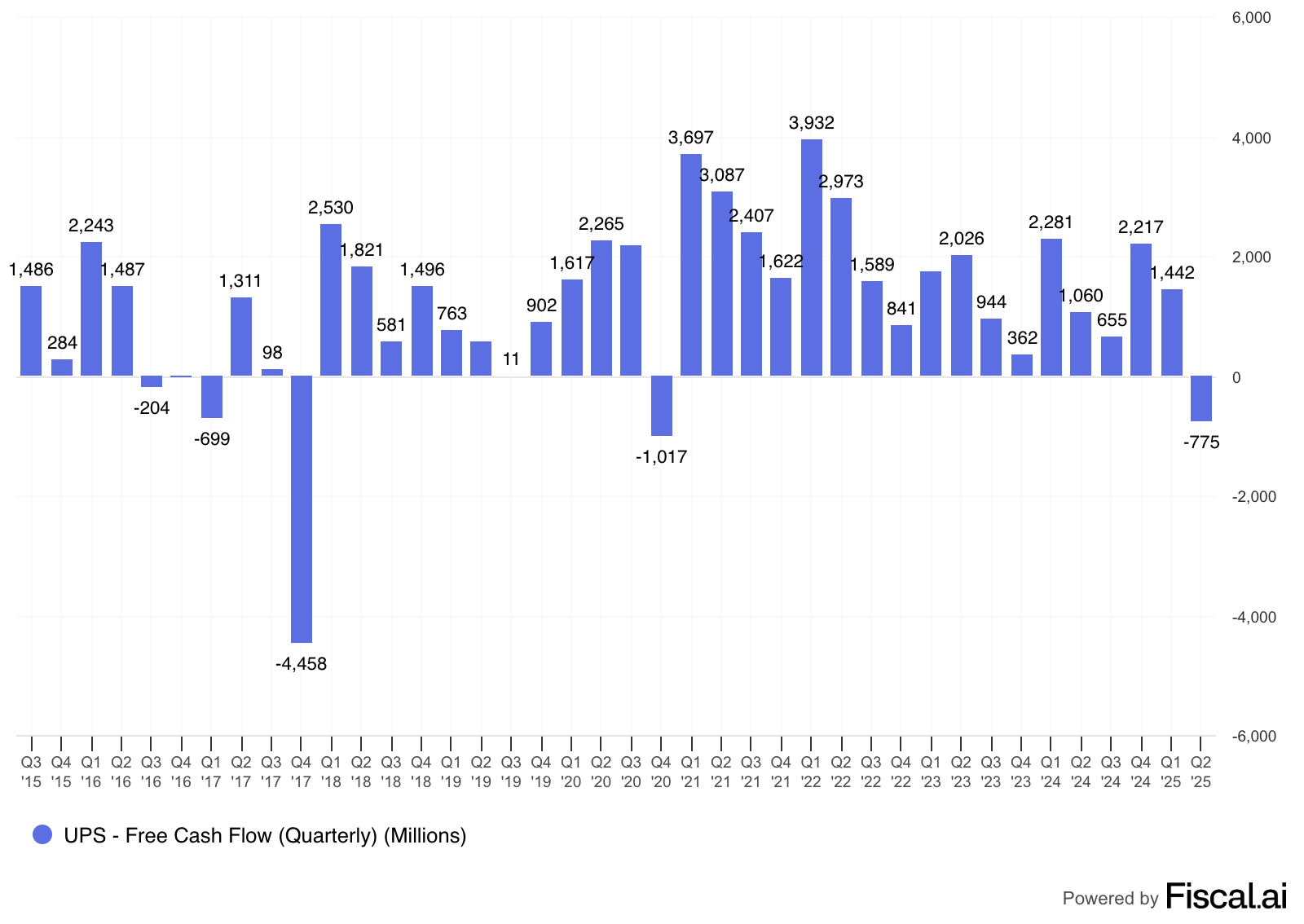

While free cash flow is tumbling...

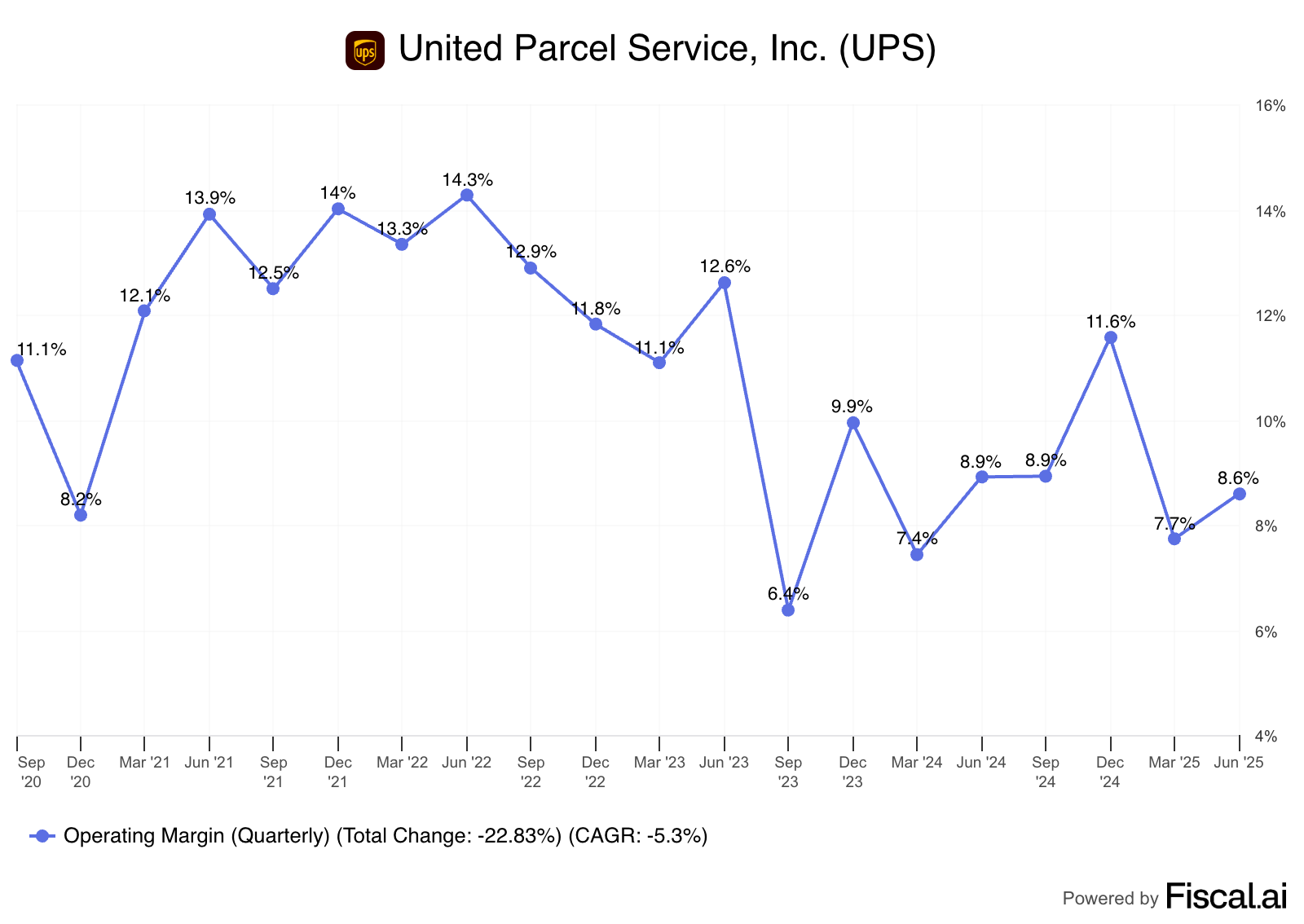

And operating margin is getting squeezed....

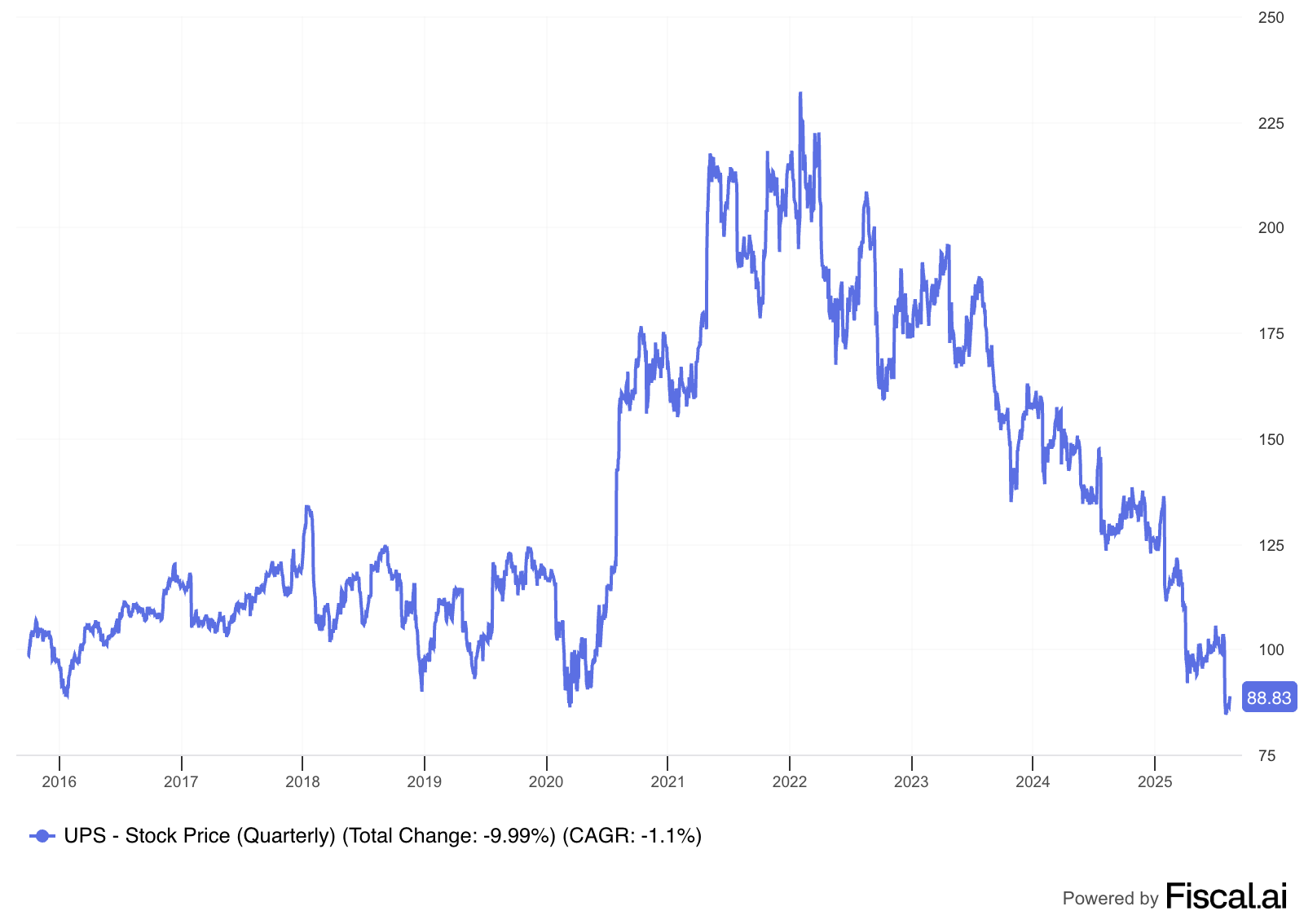

All of this is reflected in the company's stock, which along with most of its other metrics, had made UPS a star during the post-pandemic stay-at-home boom. Having a fairly new, well-liked CEO – Carol Tomé took the reins in the early days of Covid – didn’t hurt either. My, what a difference a few years make...

Concerns over a possible strike caused customers to flee and set in motion a series of events that suggests the worst is far from over for UPS. It also exposed the vulnerabilities of a business structure whose time has passed it by.

Which is where our story begins...

The Bull Case

But first the bull case, courtesy of Tenzing Memo, which I have found to be an exceptional source of getting up-to-speed on companies. This is an AI-generated summary...

UPS offers a compelling long-term investment case based on its global scale, entrenched logistics network, and strong brand. The company’s end-to-end delivery infrastructure, including a vast air and ground fleet, creates high barriers to entry and supports pricing power. UPS is actively reconfiguring its network and investing in automation, targeting $3.5 billion in annual cost savings, which should bolster margins. Its focus on higher-yielding segments—healthcare, small business, and international—positions it for profitable growth. While near-term headwinds include Amazon volume declines and labor cost inflation, UPS’s 7.5% dividend yield and reasonable valuation provide downside support. Execution on efficiency and growth initiatives is key. UPS offers attractive long-term upside if it executes on its transformation.

The Bear Case

Sounds good on paper. But make no mistake – UPS is struggling. It’s in a three-way vise:

- On one hand, it’s being squeezed by the costs and restrictive controls of having 75% of its workforce unionized, which puts it at a competitive and technological disadvantage... not to mention the constant threat of renegotiating new labor contracts. The current contract with the Teamsters, who represent most of its employees, runs for three more years.

- On the other, there’s FedEx, which has seized on its own competitive advantages – coming to the rescue of UPS workers looking for a shipper unlikely to face disruptions caused by union negotiations.

- Finally, there’s Amazon, which is increasingly becoming a competitor in its own right. And which until recently, was also UPS’s largest customer. UPS is in what it calls a “glide down relationship” with Amazon – a relationship that generated explosive growth during Covid. But earlier this year, citing the unprofitable nature of its Amazon business, UPS announced plans to accelerate the glide down to eliminate half of all Amazon’s sales by next year. By the end of this year, the company says, it should be down 30%. “That’s not a glide down,” jokes Donald Broughton of Broughton Capital. “It’s an abortion.”

Broughton knows a thing or two, here. He focuses almost exclusively on all things transportation... and has followed UPS since its 1999 IPO. He’s well connected throughout the industry, including labor, with a deep institutional knowledge.

While I had done quite a bit of research into the company in 2021 when I was doing short-biased research, especially the Amazon angle, he and I first started chatting about the company in May 2023. That was when company was negotiating yet another contract with the Teamsters, which was set to expire in July of that year. As he recalled, the negotiations five years earlier had been “a gunfight,” regardless of how negotiations this time went, he was warning that the results would “destroy shareholder value.”

Which is exactly what happened...

Built for Another Era

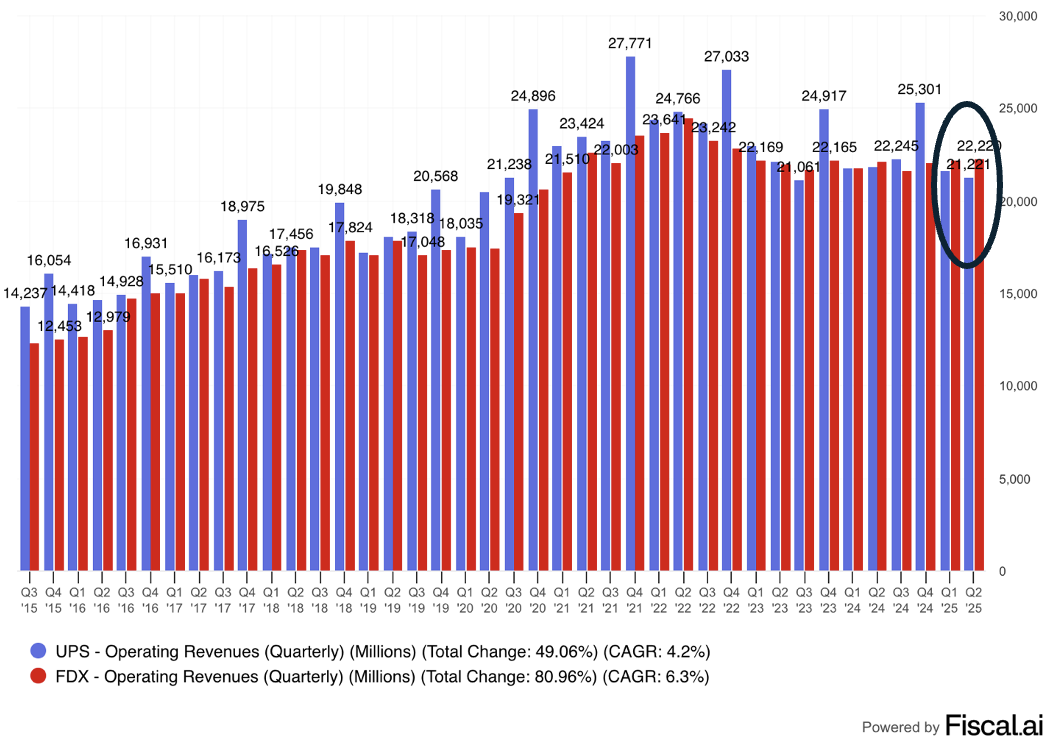

But it’s what Broughton explained when we talked a few weeks ago that convinced me that the worst is far from over for UPS, and that even with its stock having been pummeled it remains risky. A big reason is that the company is saddled with an infrastructure built for another era... one that puts it at a distinct competitive disadvantage against FedEx, which along with others – including Amazon – is seizing the moment to steal customers. That can be seen clearly in this chart, which shows how after years of trying to play catch up, FedEx’s revenues are starting to pop above UPS’s...

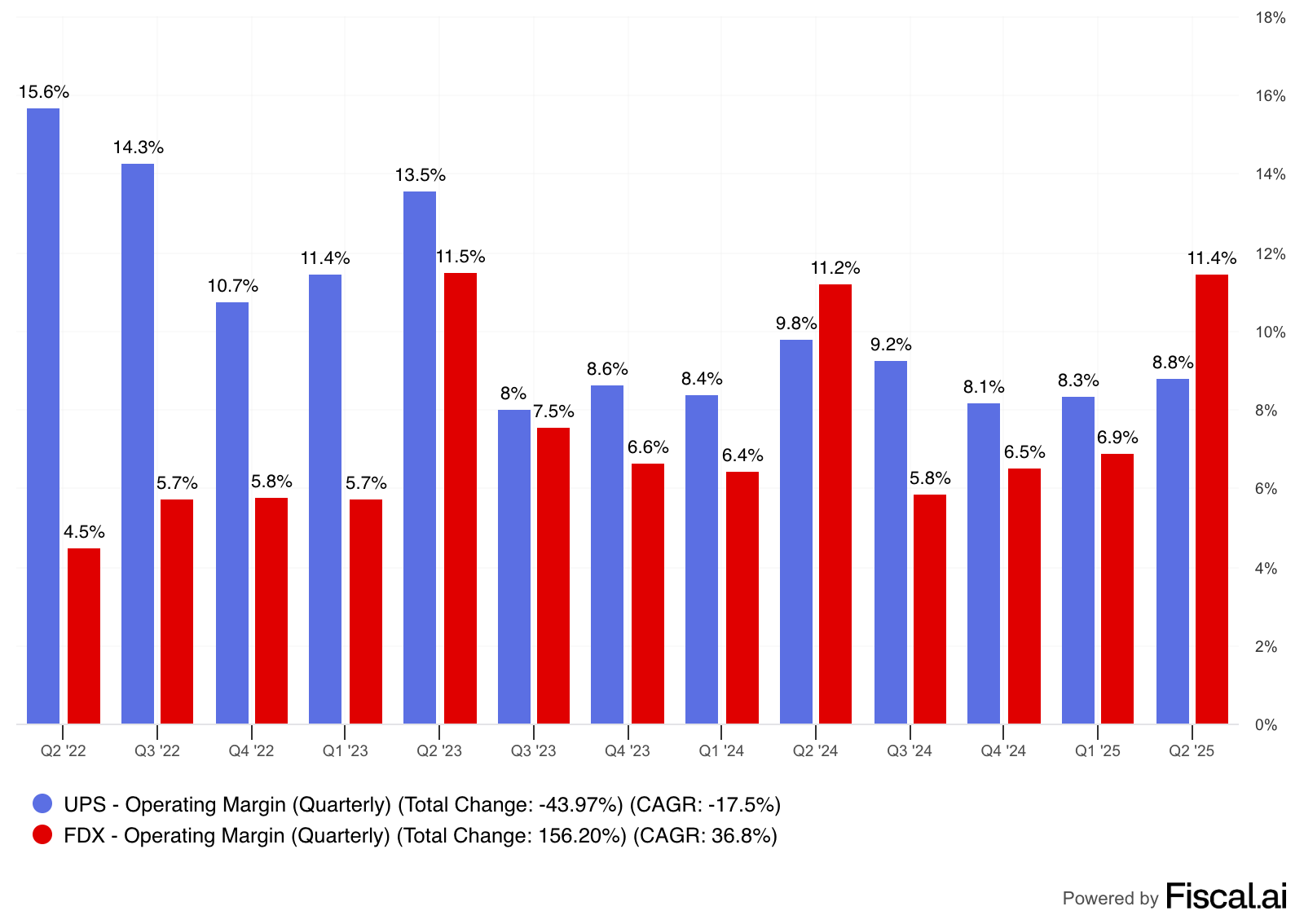

Ditto for margins, where the gap between the two companies is narrowing...

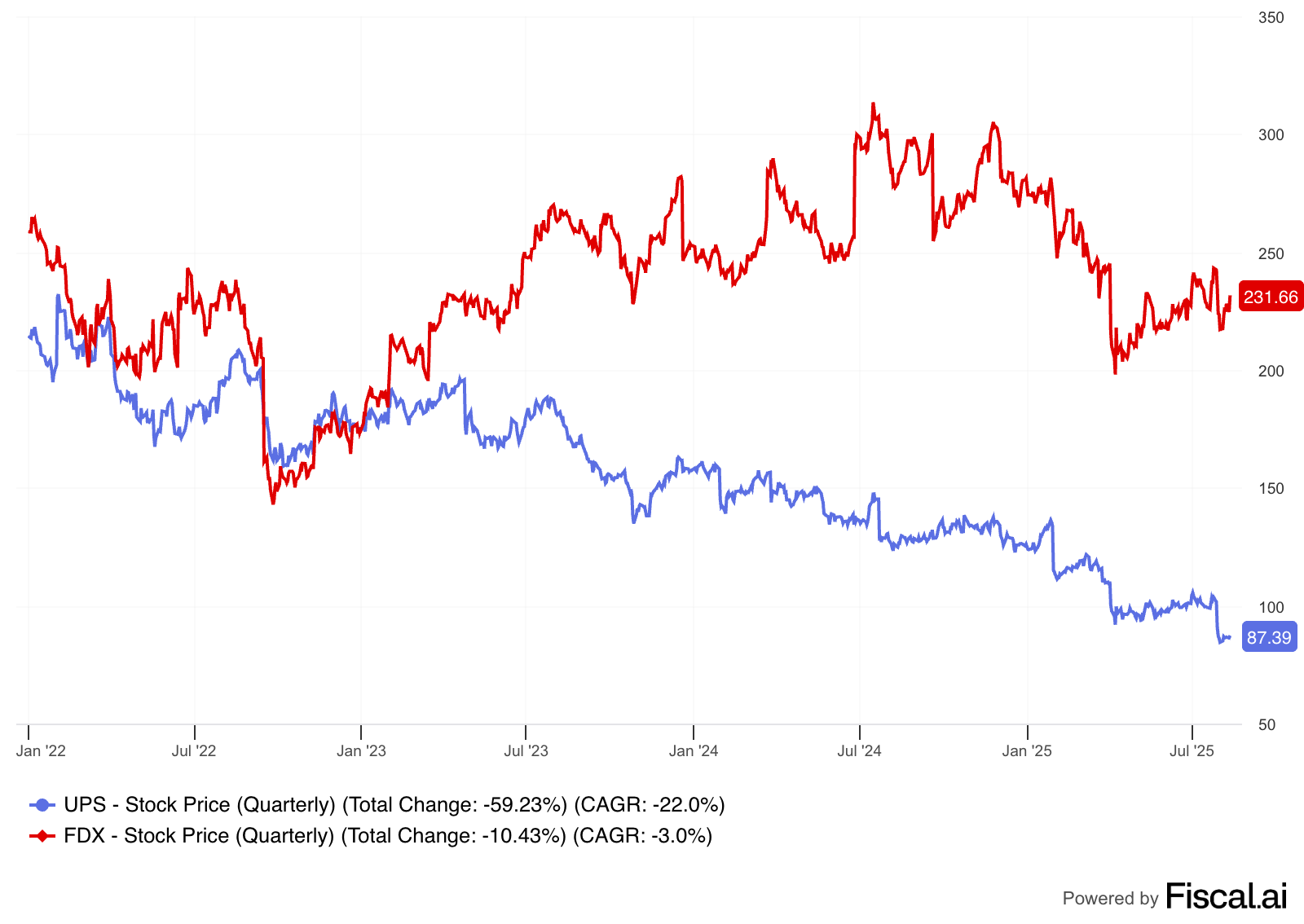

Both of those can be seen in the performance of the stocks of both since 2023, as union negotiations became a concern...

The wild card to reverse all of this is UPS’s restructuring – it refers to this as “efficiency reimagined” – which it believes will have saved the company $3.5 billion by the end of this year.