Weekly Wrap – The Moral of the Align Technology Story

Also, common sense, sham of a scam, the new gilded age and upcoming travel.

August 1, 2025

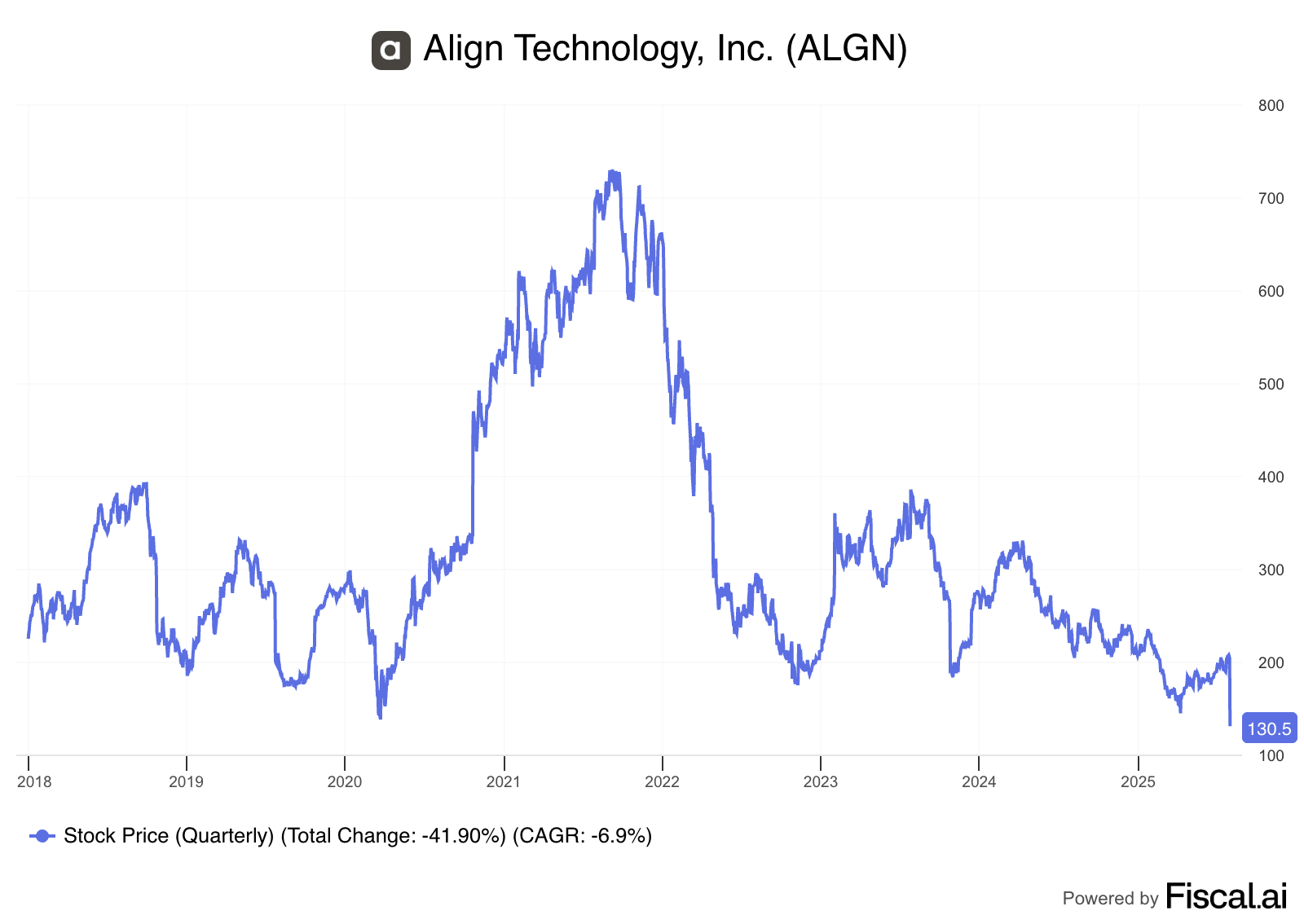

▶ I know everybody has been giddy these days, until Friday at least. But just remember what goes up... Well, they all don’t come down, certainly not immediately, but stocks that get “extended,” shall we say, at some point have their day. Look no further than Align Technology $ALGN...

Full disclosure: I’ve red-flagged Align several times over my career – and it taught me a few good lessons along the way, especially the impact of combining exceptional execution with new technologies and a solid brand... a brand seemingly every dental office had to have, no less.

But by 2018 it was starting to look stretched as revenue and case growth decelerated and competition started to increase. It looked so vulnerable that we formally initiated coverage on Align at Pacific Square Research, the short-biased research firm I cofounded. From the start it was frustrating, but still during our coverage it tumbled multiple times, once by as much as 30%, then by 50%, before Covid changed the game... and suddenly everybody staying at home wanted to fix their teeth for Zoom. The stock lifted off the launch pad, and we closed coverage in late 2020 at roughly 70% above where we started. Good thing we took our lumps and moved on, because the stock did nothing but go up and over the next 12 months Align peaked well over $700, but then did a bit of a swan dive as it turns out the pandemic merely delayed the day of reckoning. What a chart...

It has been working its way lower ever since – until Thursday, when it collapsed, tumbling nearly 40% for the day... the culmination of deteriorating trends. It’s also a likely example of what happens when the so-called “pod shops” – otherwise known as multi-strategy hedge funds, which were long and strong – say... no mas! To which a friend joked to me, “The sellside calls it ‘hate- selling.” Me to he: “What’s hate-selling?” He to me: “That’s what the youngins’ call – when you feel led on by management and you say ‘F U’ as you sell.”

Moral of the story: With these kinds of stocks that are flying, often driven by exogenous events or the narrative du jour, everybody thinks they’ll be smart enough to get out before everybody else. Maybe they will... But most won’t, thanks to human nature... as the pod shops clearly show, with all seemingly rushing to the exit at once. (At least that’s one story going around... as if anybody really knows!) And with today’s highest of high flyers, a few of which are on my Red Flag Alerts list, it should serve as a reminder of the risk. To ignore it, is foolhardy. To let it get in the way, can be a missed opportunity. But just know the market is smarter than you are. Always has been, always will be.

▶ Speaking of which... Some pearls from my friend Bob Howard – yes, him again. Bob writes the Positive Patterns newsletter. He operates from “down here in the Ozarks,” which is why he is so filled with (give it a beat)... common sense. I quote Bob a lot because he’s the perfect antidote to so much of the FOMO, YOLO, MOMO blather today. So, he says... “Some priced for perfection stocks ARE taking it on the chin this week... shows me some institutions are getting nervous. And look at the new lows list: Wendy’s, General Mills, Conagra, Procter & Gamble, Colgate. Bristol-Meyers, Chipotle, UPS LULU, OTIS - and my recently DUMPED – WFG.” And this was mid-week – before Friday's drubbing. Even old-timers like Bob, whose skill is patience, have their limits. Then again, he has owned AAON $AAON, which focuses on HVAC, since 2013 at $7 and started advising clients to start shedding some back last year when it hit $70 as it began to explode higher on the data center boom. (After all, they really need HVAC.) It was as high as $144, and as far as he’s concerned, the rest he owns is playing with house money. Going forward Bob's faves are Cement, Canada, Nuclear and Electric. He has owned cement – or rocks, as he refers to them – forever, and is the reason I own Amrize $AMRZ, the spinout from Swiss-based Holcim, ADR of which I owned until just after the split. (Hat/tip - Bob.)

▶ Speaking of markets – a bell-ringer or merely sign-o-the-times? As my regular subscribers know, my red flags over Canadian trash hauler GFLEnvironmental $GFL have themselves landed in a trash pile... as GFL has spiraled higher. Now that GFL is among the belles of the ball, despite any number of seemingly concerning risks – and despite having already smacked down the critics – if I were advising CEO Patrick Dovigi I’d advise him NOT to give this kind of interview to theWall Street Journal, in which he agreed to be front/center in this kind of feature that shows how rich he is. Yeah, I'm old school in that kinda way. Plus – it's a bad look, especially the quote at the bottom of the photo...

So you don’t need a magnifying glass, it says, “I’m trash by day, luxury properties by night.” Seems like the nouveau gilded age to moi. I can’t even...

▶ Speaking of "I can’t even...” – from the “can’t make this up” department...Ostin Technology $OST, the China tech company I flagged before it imploded, issued a press release the other day saying that its board has authorized a 1-for-25 reverse stock split. Don’t be fooled, especially when you look at the day the split is effective – August 5 – and see that the stock is suddenly $2.50. It’s an illusion. If you own $200 worth of stock, you still own $200 worth of stock. Adding insult to investor injury, the stock is so bad that this is its second reverse split in less than a year in an effort to make it look better than it really is. No wonder its stock went down by even more pennies after announcing the split. Fooled not once, but now twice, investors appear to be wising up to one of the oldest tricks in the book. Here’s the thing... Just because a company does a reverse split doesn’t mean it’s dodgy; sometimes legitimate companies that have fallen on hard times do reverse splits to boost their stocks about $5, which is a benchmark many institutions use to buy shares. But it’s almost always just another red flag atop red flags. And the fact that this trades on the NasdaqCM, which is Nasdaq’s “come one, come all” version of the Vancouver Stock Exchange – known for housing sketchy companies – is one red flag atop another. Buyer beware.

▶Speaking of reverse splits, I was going through my Red Flag Alerts list – updating pricing... and saw ChargePoint $CHPT. Last I had looked, a few weeks ago, it was trading for 53 cents, down around 95%. Now here it was, nearly $9?! Did a quick search and – yep – it did a 1-for-20 reverse split. What had been $8.55 to $0.53 is now $177 to $8.97... still down 95%... and still hanging on by a thread.

▶Speaking of shorts... Among my faves are interviews with fund managers, investors and others in the same genre. If you get a chance, take a listen to this interview former fund manager Steve Eisman did with Brad Saffalow who runs PAA Research, which does long-short research. He digs into some of his current short ideas, but goes into some of what didn’t work – and why. For folks like me who are always cognizant of the red flags, and in this go-round have been made to look like chumps a few times too many, he offered up this reminder: every great short has at least three to four rallies of 50% to 100% on the way to zero. I don’t short stocks, and am agnostic about how people trade my ideas. But when you lean heavily on the risk and see those same stocks skyrocket – when you just know how tenuous the story is – you can’t help but do a bit more than wince. I may not have money on the line... just my reputation.

▶Before we go, this head’s up: Starting the middle of next week I’ll be traveling for a month on a very long-planned trip. This is a cruise, so assuming Starlink does its thing, so will I. (It has changed the game for Internet access while on a ship.) As is usually the case when traveling, I never fully unplug. I expect to continue to write when I see something worth writing. Those who have a history with me, can attest to that. But I also need some R&R. In the meantime, if you are as much into travel as my wife and I are – and you’re a fan of travel essays – you can get a taste of where we’re going and where we have been on my wife’s travel blog – The Modern Postcard, which has been her reflection on our trips around the world. She explains our upcoming trip here. She’s an elegant writer and if you enjoy traveling as much as we do, I think you will like it. Enjoy.