Weekly Wrap – Talking Bloom, China Stock Scams, Hims, Genpact

I’ve known Paul for way too long (as in decades) and he is nothing if not direct (never shy to speak his mind, including telling me – to my face – when he thinks I’m wrong.) I always listen, because he also happens to know more about tech investing than most. But he has extra credibility with me because unlike many of his peers, he also likes short-selling, and likes nothing more than sniffing out a truly scammy company.

By the time he contacted me, Paul had been long Bloom since 2019, having originally bought it at an average price of $2.25. (It’s now nearly $70.) While I didn’t quote him by name, I went on to share his thoughts as a counter-point. You can read them here. What really struck me was what Paul volunteered at the tail-end of his comments...

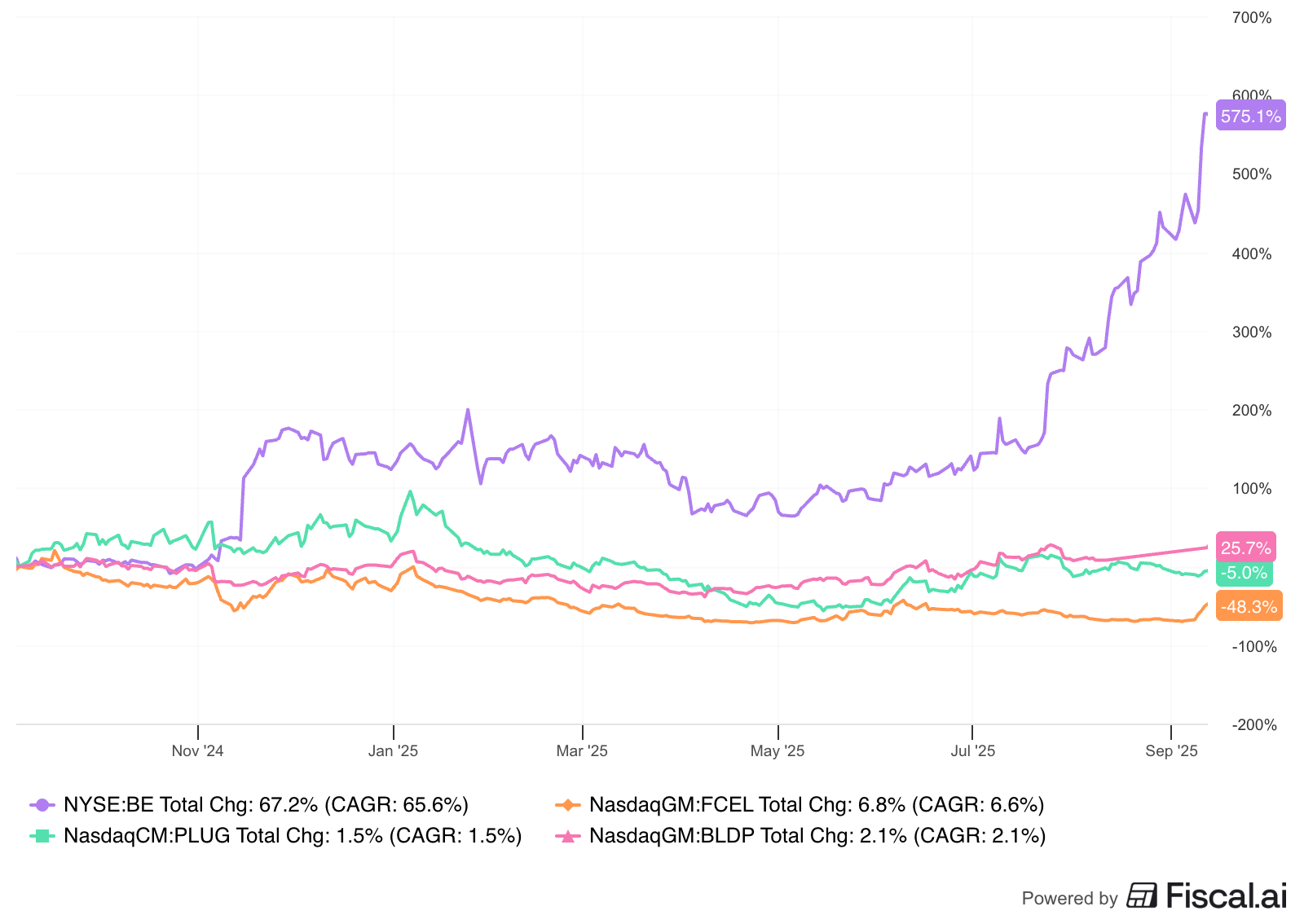

Not a name to bet against, given electricity shortages and Bloom’s best in class efficiency (60% plus). Bloom is not PLUG or FCEL or BLDP.

PLUG or FCEL or BLDP? Like Bloom, all three of those – Plug Power, FuelCell Energy and Ballard Power – had become extreme battlegrounds. That Paul had specifically called them out was striking, especially looking back. Here’s how they all have done since then. Bloom is the purple line...

Which gets us to today. A few weeks ago I had pinged Paul on something I had seen him post on social media about rise in grift...

I responded in the thread, writing... “Golden Age of... oh, never mind!” I sent him a follow-up note. He thanked me and added, “Have you been watching Bloom?” I hadn’t, but took a peek and saw the stock had exploded sharply higher. And as it turns out, Paul's firm now owns a 20% stake. While Bloom still has to start making money, I wondered what Paul saw so early that made him believe that Bloom would be – and still is – the one he would bet on. He responded...

They had a great product, truly unique with great IP; it's a huge market; they were succeeding in lowering COGS by 10% per year; margins were steadily improving; they were winning a lot of new customers; and they were committed to quickly becoming profitable and FCF positive. They had ugly cash flow and a receivable issue with an AMZN data center that the greenies in OR wouldn't release a permit for, but we trusted management that these issues were transient...and they were correct.

He then added...

Bloom has had some board members and execs that we've trusted and felt were exceptional people....old CFO Randy Furr was CFO of Spansion Semi (we were top holder; sold to Cypress Semiconductor at great price); John Chambers and Mike Boskin are on the board, as is Jeff Immelt. And CEO KR Sridar had never sold any stock....

Meanwhile, short interest in the company, while down from its highs – actually, it’s the lowest it has been all year, suggesting capitulation by shorts – is still at around 20% of the float. That puts it in the top quartile of the short-squeeze list by my friends at All Star Charts. To which I say: Interpret at will.

▶A word about short squeezes... Like them, hate them or play them, squeezes are part of the market. I cringe when I see a name I’ve red-flagged getting squeezed, but it’s been that way as long as I’ve been doing this... and that’s decades. The difference now is the squeezes are on steroids. The reason, as one friend who runs his own money and goes long and shorts observes, “With Pod shops getting so much of the capital, then leveraging it – and trying to be market neutral by the end of every day – by definition they press when shorts are down and have to cover when up.” Now, with Robinhood starting to offer short-selling, this could get interesting... or maybe I should say, more interesting. I’m just waiting to see the retail-orchestrated bear raids, which by the way, kids – if you’re thinking about marshalling your (fill-in-the-blank) “army” to do it – is illegal. Stay tuned.

▶Speaking of THIS stock market... If you missed my report yesterday on why this is a “throw-a-dart” market – featuring my pal Mr. Muggs the chimp – you can read it here.

▶Speaking of chimps... One stock red-flagged, which has made a chimp out of me (so far!), is Hims & Hers $HIMS, which is best known for selling knock-off ED, baldness and GLP-1 drugs online. Yesterday Marty Makary, the commissioner of Food and Drugs at the FDA, wrote an op-ed in the New York Times going after drug advertising. Among his comments, the one that caught my attention...

▶Finally, show me the money... Whenever I see big deals announced these days, like the $300 BILLION deal between Oracle $ORCL and OpenAi, I always think... Who's got that kinda cash? I’m not alone, the best take on this was by Gary Marcus who writes on AI at Substack. From his piece....

- OpenAI doesn’t have $300 billion dollars

- They don’t have anywhere near $300 billion dollars

- By their own (presumably optimistic) projection, they won’t turn a profit until 2030.

- And all this from a company thought (or claimed) that GPT-5 was going to be tantamount to AGI (spoiler alert: it wasn’t)

- For good measure Oracle doesn’t have the chips they would need to fulfill the contracts, or even the cash to buy them.

I won’t say that it is all make-believe, but, well, you do the math. (Did people promising to build potential future greenhouses for tulip-growers in 1636 ever have it so good?)

If Oracle actually collects its $300 billion, I will truly be astounded.

Nothing I can add. The beat goes on...

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice. (Because it isn’t!) I don't own any stock mentioned in this report.

Feel free to contact me at herb@herbgreenberg.com