Michael Saylor, tl;dr: 'Just Trust Me.'

I've seen and heard a lot; this latest infomercial by Strategy for its preferred stock takes the cake.

One take-it-to-the-bank rule-of-thumb of investing and Wall Street is that the higher the yield, the higher the risk.

Another is that if it’s too good to be true, it usually is.

Worse, if it’s being pitched as if it’s the next-best thing to risk-free, it usually isn’t.

The wild card is when the pitchman is Michael Saylor of Strategy (née MicroStrategy) MSTR 0.00%↑, when he’s talking anything bitcoin-related, but especially what he calls “digital credit.”

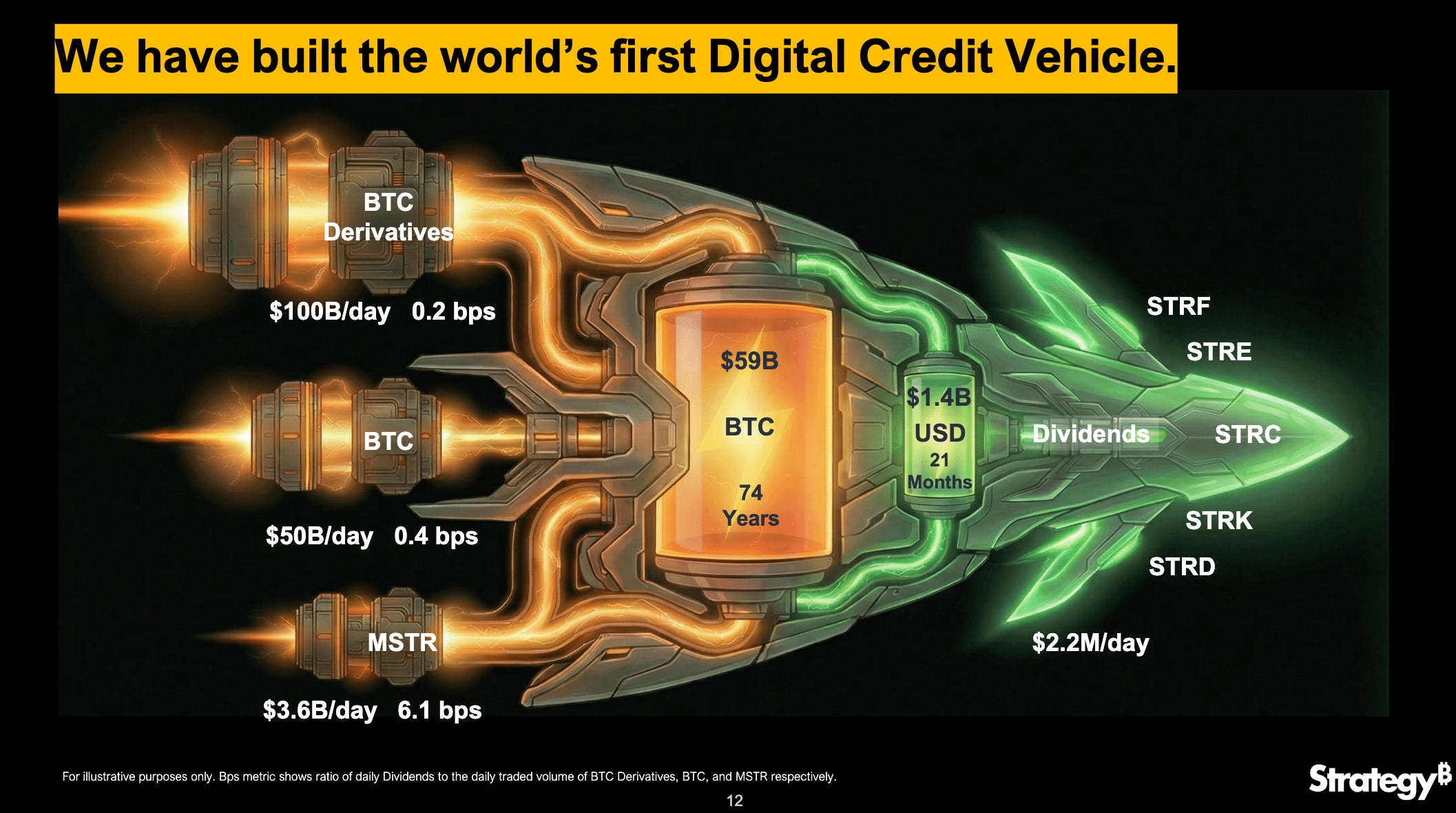

Never mind that there’s no such thing as digital credit as a security. But that hasn’t stopped Saylor from talking about it nonstop, starting mid-last year, as if digital credit were common knowledge rather than a made-up marketing wrapper used to sell his latest financially engineered concoctions… created for the sole purpose of financing Strategy’s purchase of more bitcoin. “Big innovation,” is the way he has described it. It’s so big that “digital credit” was mentioned a record 48 times during scripted comments by management on the company’s latest earnings call, with 37 mentions – the most ever – in the earnings presentation, including this one…

Like most of Strategy’s earnings and investor calls, this one was part revival meeting, part traveling medicine show, and part Advertising/Marketing 101 – pulled directly from the “tell them what you want them to hear and think” school of salesmanship. (Think Mad Men’s Don Draper turning Kodak’s drab-sounding slide projector “wheel” into a “Carousel” of memories.)

Saylor’s approach is either brilliant or brilliantly devious or deviously deceptive, depending on which side of the bitcoin and more specifically – Strategy – divide you’re on. Or as the New York Times recently wondered, in an article in which I’m quoted…

I’ll let you debate that question, bitcoin, and all other Strategy matters among yourselves.

What I do know is that if you eliminate the name of the company or the person saying it and just go merely on what has and is being said – especially on this last earnings call – you might consider holding on to your wallet.

Here’s why…