New Red Flag Alert – The Sudden Surge in AXT

Perhaps no company exemplifies the silly late-stage nature of this phase of the AI gold rush.

Some companies are simply begging to be red-flagged. Such as AXT Inc.AXTI 0.00%↑ …

AXT is one of those companies that has attracted whatever is left of the YOLO crowd, even if the substance doesn’t match the story. It reminds me in every way of so many other companies that had their moment in the stock market sun, swept up by real or perceived potential new business from the narrative du jour.

That narrative today is that, as the construction of AI‑centric data centers has boomed, so has the demand for advanced fiber optic connectors, which rely on indium phosphide lasers to deliver the required speed.

Guess who makes critical indium phosphide substrate wafers used to make the lasers?

You got it – AXT.

It’s quite a story… and I stress… story. Perhaps no company exemplifies the silly late-stage nature of this phase of the AI gold rush more than AXT, which appears to be little more than a microcap MOMO trade gone wild… more of a throwback to the latest round of AI FOMO.

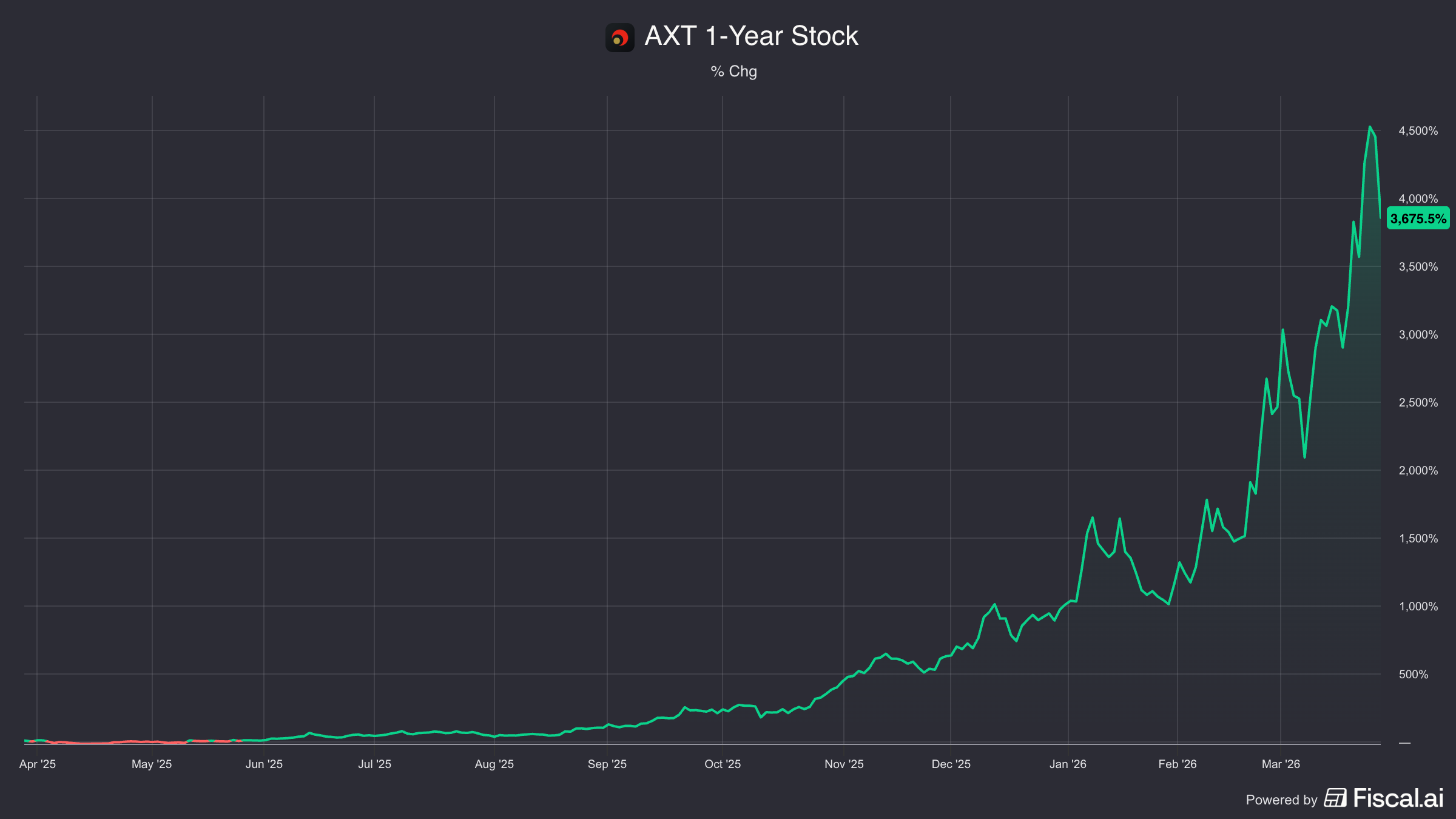

This is, after all, a stock that as recently as last spring traded just above $1, with a market value of $60 million before taking off. It’s now $60 with a market cap of $3.3 billion.

But beyond its market value and stock price, AXT still has all the hallmarks of the microcap it really is… and not just because its board of directors is comprised of three outsiders and the CEO.

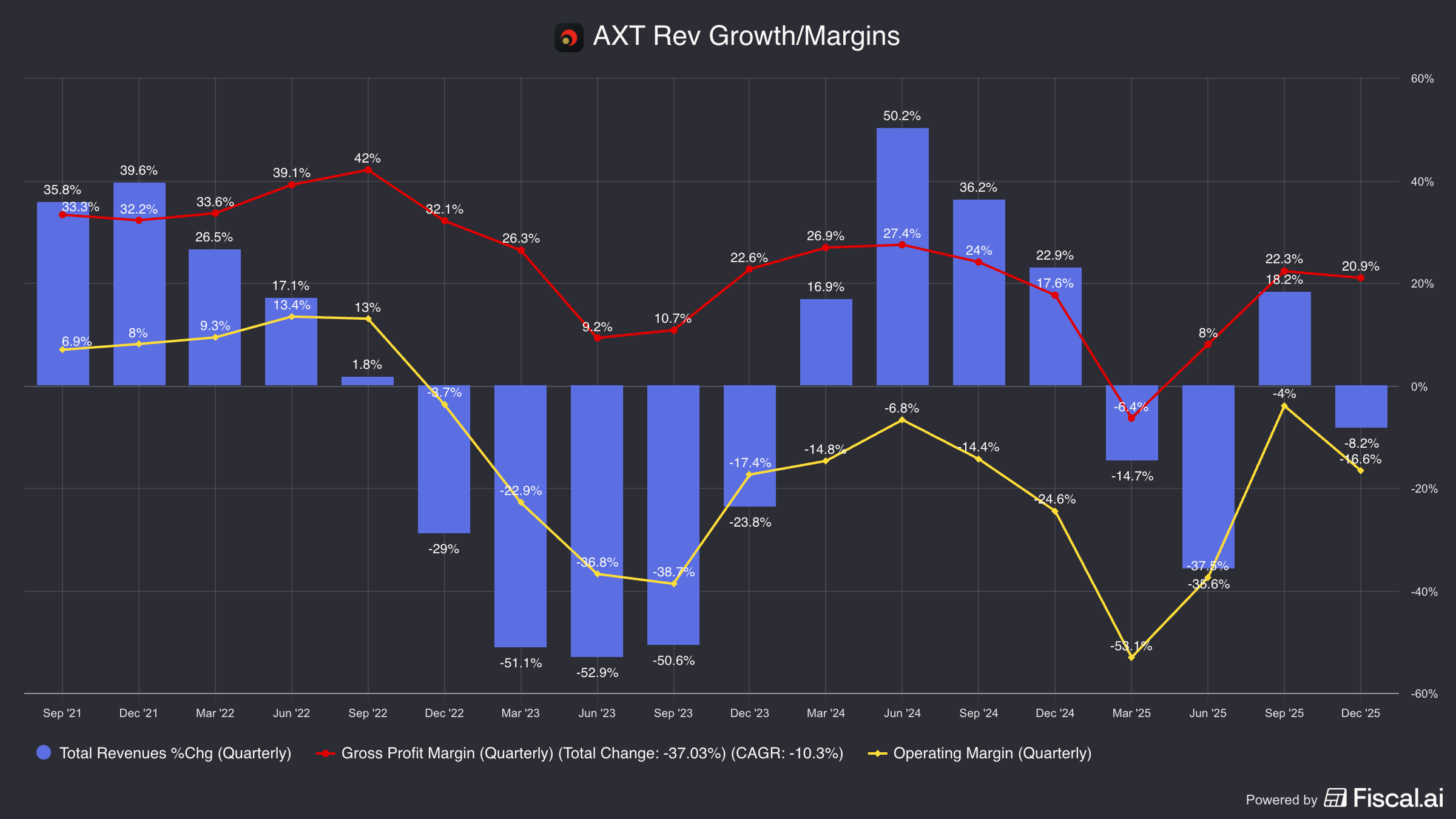

And it has the financial performance to match, with muddling revenue growth and margins…

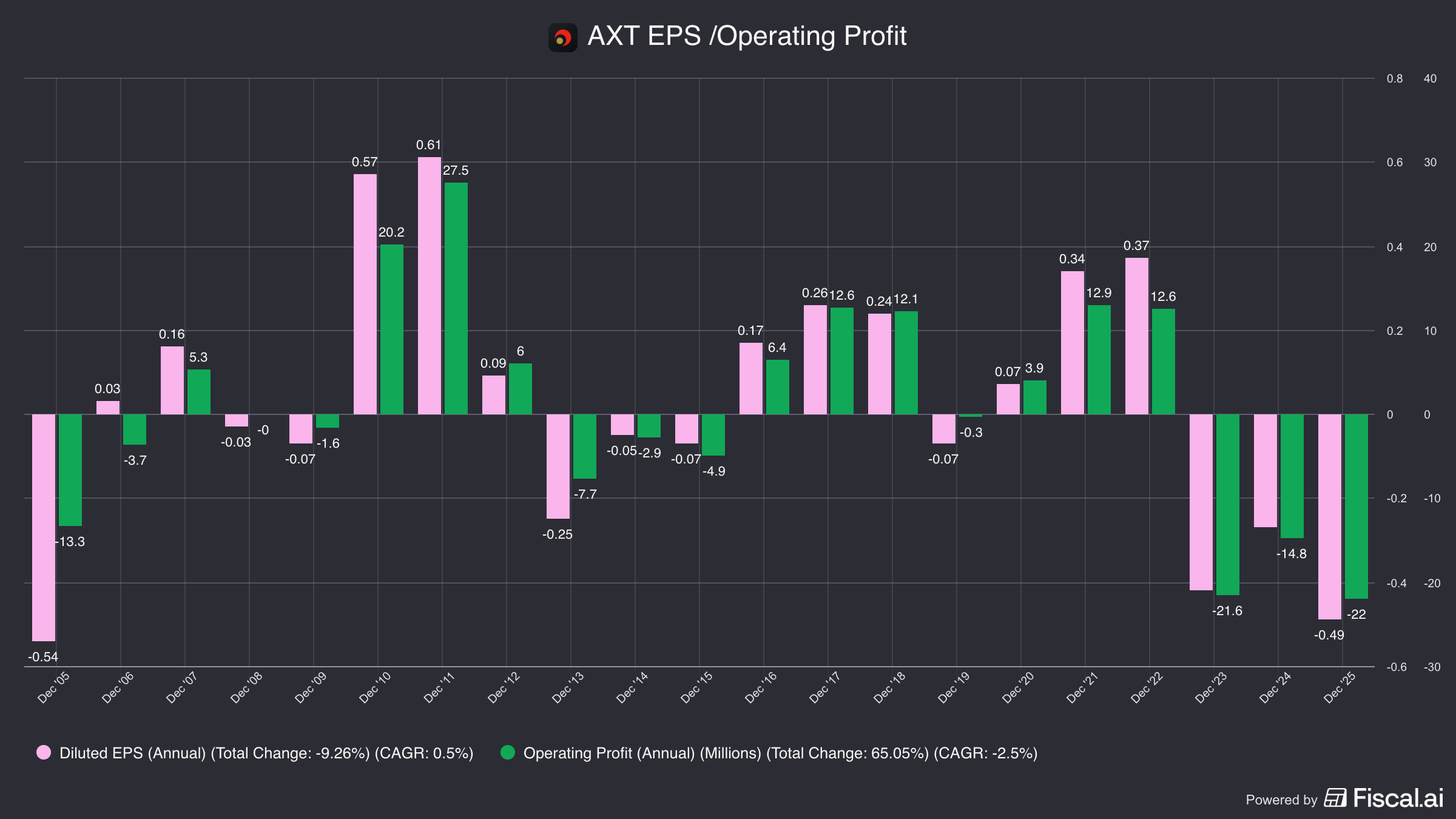

And even after being in business for 40 years, its ability to make money has at best been spotty…

To the bulls, of course, that’s looking backwards.

Bull Case

For them, it’s what’s coming next for a company they believe is in the right place with the right product at the right time. Here’s an AI-generated summary of what has been driving the stock… courtesy of my friends at Tenzing MEMO…

AXTI is a levered way to invest in one of the least-appreciated choke points in AI infrastructure: indium phosphide (InP) substrate wafers, a critical input for the lasers and detectors used in high-speed optical links inside and between AI data centers. As compute scales, optical connectivity becomes more important, and AXTI sits upstream in a technically difficult market with only a few qualified suppliers.

The near-term numbers look messy, but the bull case is that 2025 was distorted by export permit delays and temporary manufacturing issues, not by weak demand. Management has described backlog above $60 million, expects sequential growth in Q1 2026, and is seeing especially strong InP demand tied to AI buildouts. If permits continue to improve, delayed orders can quickly convert into revenue.

There is also significant operating leverage here. AXTI’s margin collapse came from low utilization and bad product mix; if InP shipments normalize and capacity fills, gross margin can recover sharply. Meanwhile, the December 2025 equity raise added about $100 million gross, leaving the company with roughly $120 million of cash at year-end and a net cash position, which gives it time to expand capacity.

In short: scarce product, real AI demand, limited competition, improving liquidity, and potentially explosive earnings recovery if regulatory friction eases.

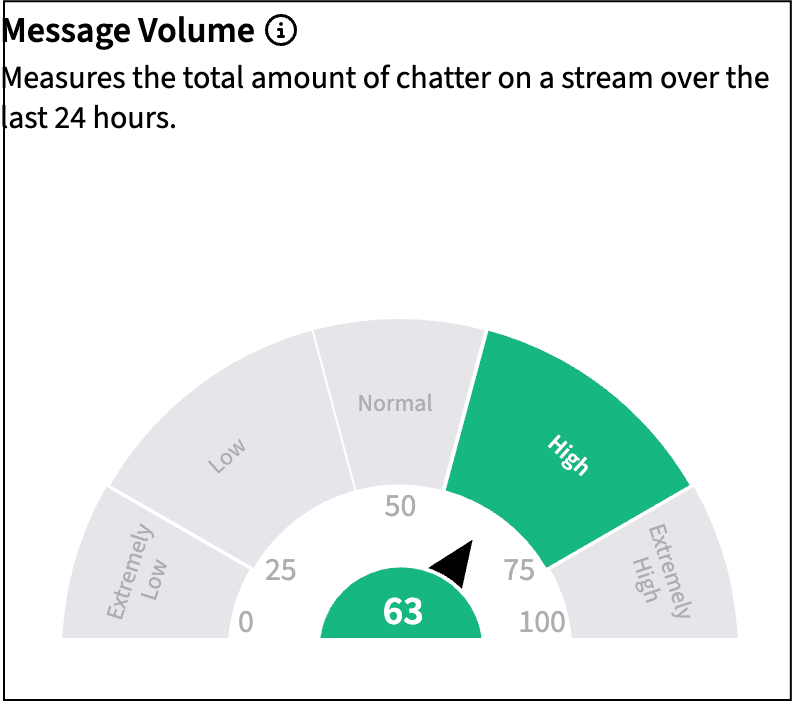

Based on my research, that’s the story, at least, and that’s why there is no shortage of social media chatter on AXT, as seen here via Stocktwits…

But as is often the case with stocks like these, there’s the story, and there’s reality… and reality is that while AXT is a potential winner in the booming demand for indium phosphide substrates, the story ain’t all the stock suggests it’s cracked up to be.