Red Flag Radar: ‘Irrational Extrapolation’

What happens when one ‘Sideline Critic’ takes on RH

(This friendly reminder: My Red Flag Alerts and selected On the Street content are no longer free. But while the paint is still drying on my paywall, my introductory price remains. I will be raising prices. Here’s more on my decision to go paid, and what to expect from my Red Flag Alerts.)

Here’s something you don’t see every day: an analyst taking on a company in a public forum... for all to see.

That’s what my friend Rob Wilson of Tiburon Research – in his Consumer EQ newsletter – has been doing lately with RH RH 0.00%↑, the old Restoration Hardware, where he is a former treasurer.

I’ve been quoting Rob for well over a decade for a simple reason: He’s not afraid to say publicly, for attribution, what he’s thinking based on his analysis of the earnings call transcripts, filings and his own exceptionally deep models.

They lead him to ask more thoughtful, detailed and direct questions than the average analyst of the 40 consumer companies he tracks. No surprise, most companies don’t respond when he reaches out. “I almost feel like a prosecutor instead of an analyst,” he jokes.

‘A Complete Dud’

Among those who don’t respond: RH.

Our story begins with the company’s second quarter earnings a few weeks ago...

Reported results were mediocre, but the stock shot up more than 30% since then – more than 40% at one point.

The reason: Friedman’s comments on the call, which were akin to a victory lap, as he proclaimed…

The company is gaining market share.

Its outperforming the industry by 15 to 25 points.

Performance should gain momentum in the second half.

But it was this comment by Friedman that really got Rob’s attention...

A lot of reasons why we will take a lot of market share. I mean, it's not an accident, right.

I mean, we've been talking about this a long time. The question was, well, when will it happen?

I mean, some guy that I know – that used to work here as an analyst – put out a report last week, never talked to me. I don't know, probably 15 years, and he said, ‘Oh, the product transformation is a complete dud.’

I don't know how he feels today, but you can feel worse in the coming quarters. You don't learn anything by being a sideline critic. If you want to learn something, come here and ask some questions and you'll learn something.

If you're going to be a sideline critic, you're not going to learn a lot. And you'd be wrong a lot more than you're right.

Rob suspects that the “some guy” Friedman was referring to was him, since just a few days earlier he had put out a note that said...

The product ‘transformation’ which began in Fall 2023 has largely been a dud.

He still thinks that’s the case and doesn’t think Friedman is telling the complete story.

Why? Let’s take a closer look at his broader analysis, the questions he has forwarded to the company, along with comments he told me when we chatted earlier this week...

As outlined in his Consumer EQ, Rob’s key points include...

Claims of market share gains are disingenuous.

Ad spend isn’t really paying off.

Inventory is bloated.

European expansion will be a challenge.

But before we go there, context is important...

The Second Coming

Many people forget that the current iteration of RH is really the second coming of the company, which originally went public in 1998.

I often use Restoration Hardware as an example of a company that had no business going public, but was lured into an IPO by eager bankers as the dot-com bubble gave any and every company willing to take the bait a free pass to cash in.

At the time, Restoration Hardware – or RSTO, as its symbol was back then – was a hot regional concept in the Bay Area. But like so many other hot regional retail concepts, it simply didn’t travel well, rapidly expanding nationally as a mall-based retailer to meet the street’s aggressive growth expectations.

For Restoration Hardware, that meant a near-brush with bankruptcy, until it went private in 2008, in a deal that included CEO Gary Friedman…

By the time the company IPO’d again in 2012, Friedman had already begun transforming what would now be known as the “RH brand” from just another mall-based retailer into a “luxury lifestyle brand” dominated by free-standing “design galleries.” The new stores, the company initially said, would be 20,000 to 60,000 square feet, compared with the average store that was around 7,000.

Merchandising Wizard

It was a gutsy move, or as Friedman recalled on a recent earnings call...

For the past 23 years, we've heard others tell us what can't be done. And for the past 23 years, we failed to listen. We avoided bankruptcy while being accused of lunacy.

Known for taking big risks from early in his career, Friedman had built a reputation of being somewhat of a merchandising and marketing wizard.

And by 2013, with revenue of barely $1 billion, he expanded the transformation narrative to include forecasts that RH’s “long-term potential” would make it a $4 billion to $5 billion brand.

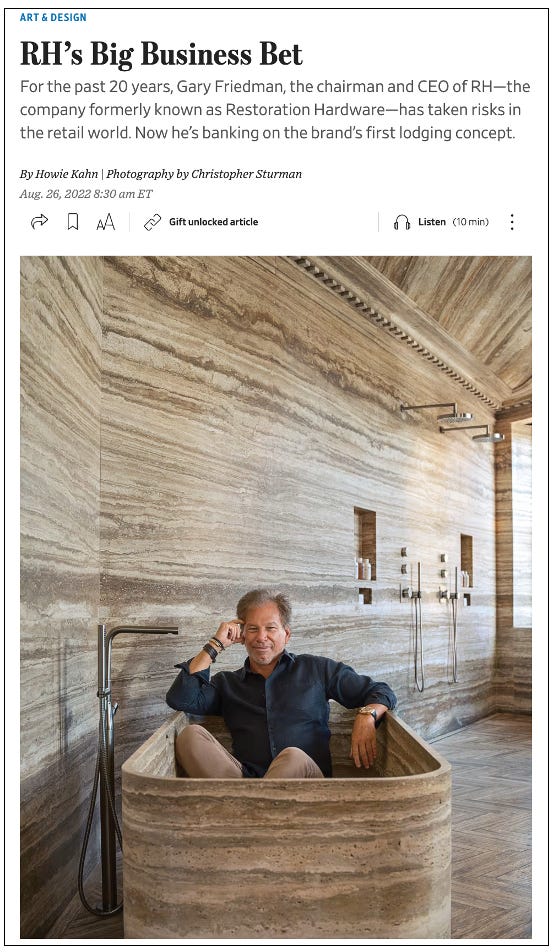

RH, which officially changed its name to Restoration Hardware in 2017, has even gotten into lodging and restaurants. The Wall Street Journal called the move “RH’s Big Business Bet.”

As Rob puts it…

His thesis was a masterstroke from an investor relations perspective. He starts to open these larger stores and he convinces longs to extrapolate those results into the future when most of the country is dotted with these larger stores.

Investors liked what they heard, and as the RH’s aesthetic steamrolled through the home furnishings industry, the story Friedman was telling steamrolled through Wall Street, flattening short-sellers in the process.

Tug-of-War

Rob attributes the stock’s performance and the subsequent long-running bull/bear tug-of-war to what he likes to call “irrational extrapolation” by analysts who bought into Friedman’s thesis.

Or as he explains...

That's why, as you say, the shorts got crushed. Extrapolation is a difficult concept to disprove at earlier stages.

Especially when things look like they might be working, which was the case after the first design center opened in 2014, with revenue for the entire company near-doubling over two years.

But by the end of 2015 growth had stalled and the stock tumbled, staying down until 2017 when despite unimpressive revenue growth operating profits exploded higher.

Then came the post-pandemic bonanza of all things home furnishings, with RH’s revenue and operating profit reaching record highs in fiscal 2021... including operating margins, which rose to 26.5% from the teens.

Things were going so well that in mid-2020 the company upped its long-term revenue forecast to between $5 billion and $6 billion in North America, with worldwide revenues eventually topping $20 billion… and that’s with revenue still $1 billion shy of the $4 billion target forecast more than a decade earlier.

But by 2022, things started to unravel, with sales, profits and margins tumbling... even as the company was in the middle of opening galleries in Europe.

In response, RH rolled out what it called its “most prolific product transformation” ever as it “climbs up the luxury mountain.”

Market Share Magic

Which gets us to where we are now, and why Rob is so worked up...