The Wrap – ETFs and Systemic Risk

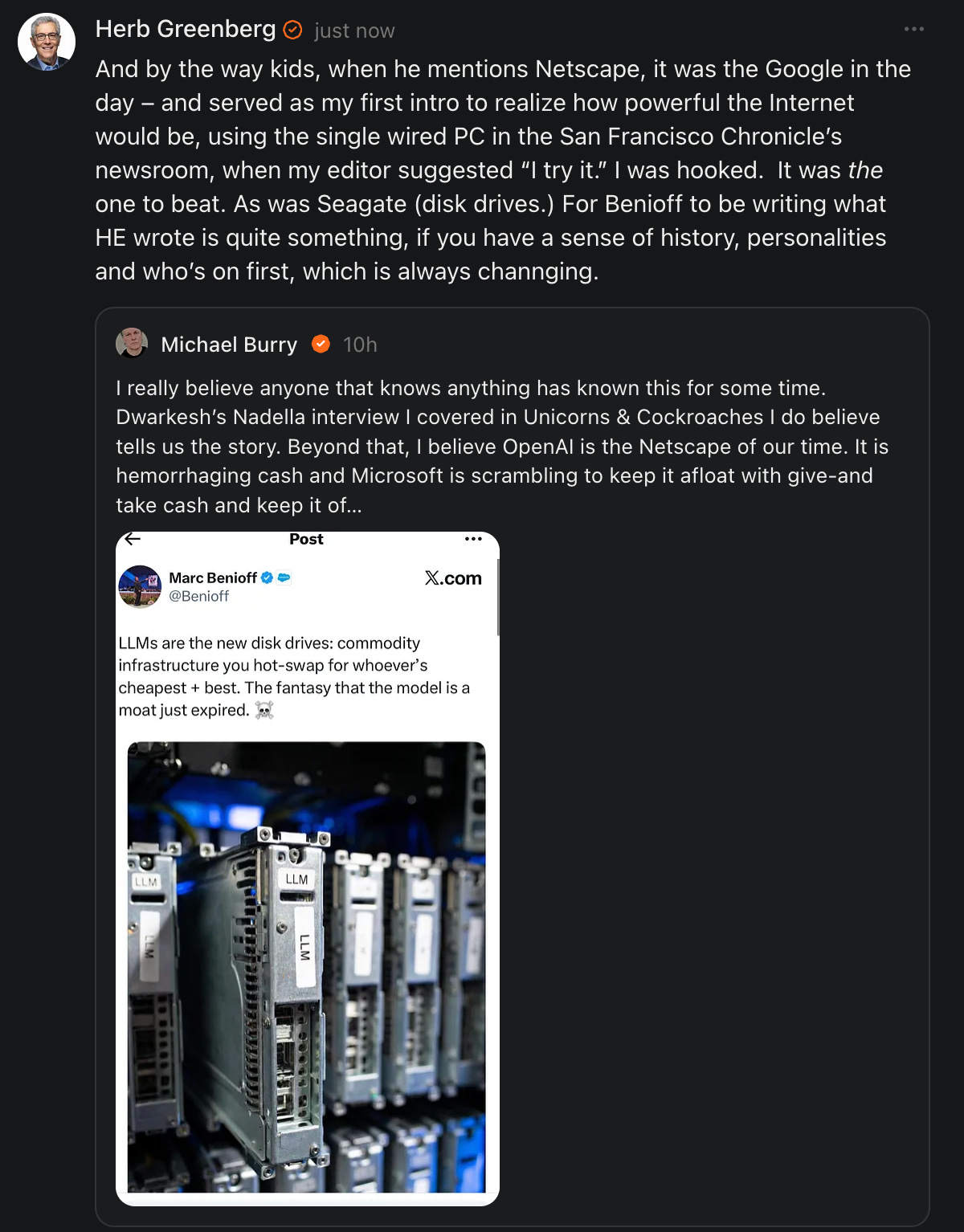

Also, for premium subscribers – is this another canary in the AI data center mine?

Special thanks to Tenzing Memo, FinTool , ManagementTrack and Fiscal.ai, whose tools play an integral role in my research.

This report includes content exclusively for premium subscribers. I don’t do Black Friday or Cyber Monday specials. MY PRICES ARE RISING SOON. If you’re not yet a premium subscriber to Red Flag Alerts, becoming one is easy. Simply click here…

1. No Longer JUST the Tail Wagging the Dog

Finally (if you haven’t heard), the SEC is looking at leveraged ETFS, with a halt on reviews – let alone approvals – of any ETF levered more than two times. Small steps! But it got me thinking: 15 years ago, when I was senior stocks commentator at CNBC, I wrote about about a new study on the downside of ETFs – notably, the potential systemic risk they posed. It was tied to a report from a few guys who hadn’t just fallen off a turnip truck.

Among their concern was that ETFs would hurt the creation of IPOs (check); that there would be lax oversight of them (check); that the ease of shorting them would make them ideal triggers for market-wide free-falls (who knows); and that contrary to popular opinion, they’re really little more than derivatives (check.)

As you might guess, it sparked quite a bit of backlash, but I followed up the next day with another article – again, based on the same report – suggesting that ETFs were really just another form of financial engineering. Since then, ETFs, of course, have gone on to be not just “the tail wagging the dog” of the market, as I had written, but to become the market.

As John Authers of Bloomberg writes in a piece headlined, “Your ETF is Ruining Capitalism”…

Exchange-traded funds have only existed for a little more than three decades. The first US ETF launched in 1993. By the end of 2008, the year of the crisis, US-based ETFs held $538 billion. That is now above $9 trillion, far exceeding the gain for Wall Street equities, and up some sevenfold over the period.

Proliferation is such that there are now more ETFs than there are listed stocks. Indexes, once designed to simplify the job of investors and help gauge overall market trends, have ballooned even more. There’s no precise census of all the financial indexes available, but they plainly dwarf the total number of stocks or bonds available anywhere on the planet.

His report focuses on a book by Columbia economist Amar Bhide, which seems to argue that financial derivatives, especially in their standardized, highly-traded forms, exemplify how modern finance has drifted away from judgment and toward mechanical risk engineering. “Financial engineering,” Authers writes, “has created a baffling array of products making any number of formerly illiquid assets — from mortgages through infrastructure projects to reinsurance contracts to foodstuffs — into instruments that can be traded in fast-flowing markets.” Or as I like to think of it, creating derivatives out of everything and anything, even if they’re nailed down.

He then goes through a brief history of the creation of ETFs and how they clash with various economic theories – and goes on to write…

Their proliferation now encourages a top-down approach, divorced from individual companies. Liquid markets allow numerous ETFs to trade, and operate different strategies, with their trading often driving movement in the underlying companies — not the other way around.

“There comes a point when innovative financing is in fact not much more than placing one piece of paper on top of another piece of paper,” says Viktor Shvets of Macquarie Capital, whose book The Twilight Before the Storm warns of the parallels between capitalism’s current difficulties and the crisis of the 1930s. He also warns that it may now be too late to try to redress the balance as the financial superstructure has been allowed to grow so much larger than the underlying real economy.

Or, put more simply: That rocket ain’t coming back to the launchpad.

P.S.: Cue my pal Dave Nadig, who is president and research director of ETF.com. He thoroughly disagreed with the research paper 15 years ago, and while he’s as opposed to highly levered ETFs as many if not most, I’m sure he’ll have a few choice words to say here. (Oh, and by the way – yes, I own ETFs. But I also own stocks.)

2. Random Thoughts

A few knee-jerk moments from the week…

And just for fun, a bit of fun reality…