The Wrap – Jump the Shark Moment for RH?

Plus... AXT and updates on Progress Software and Turning Point Brands.

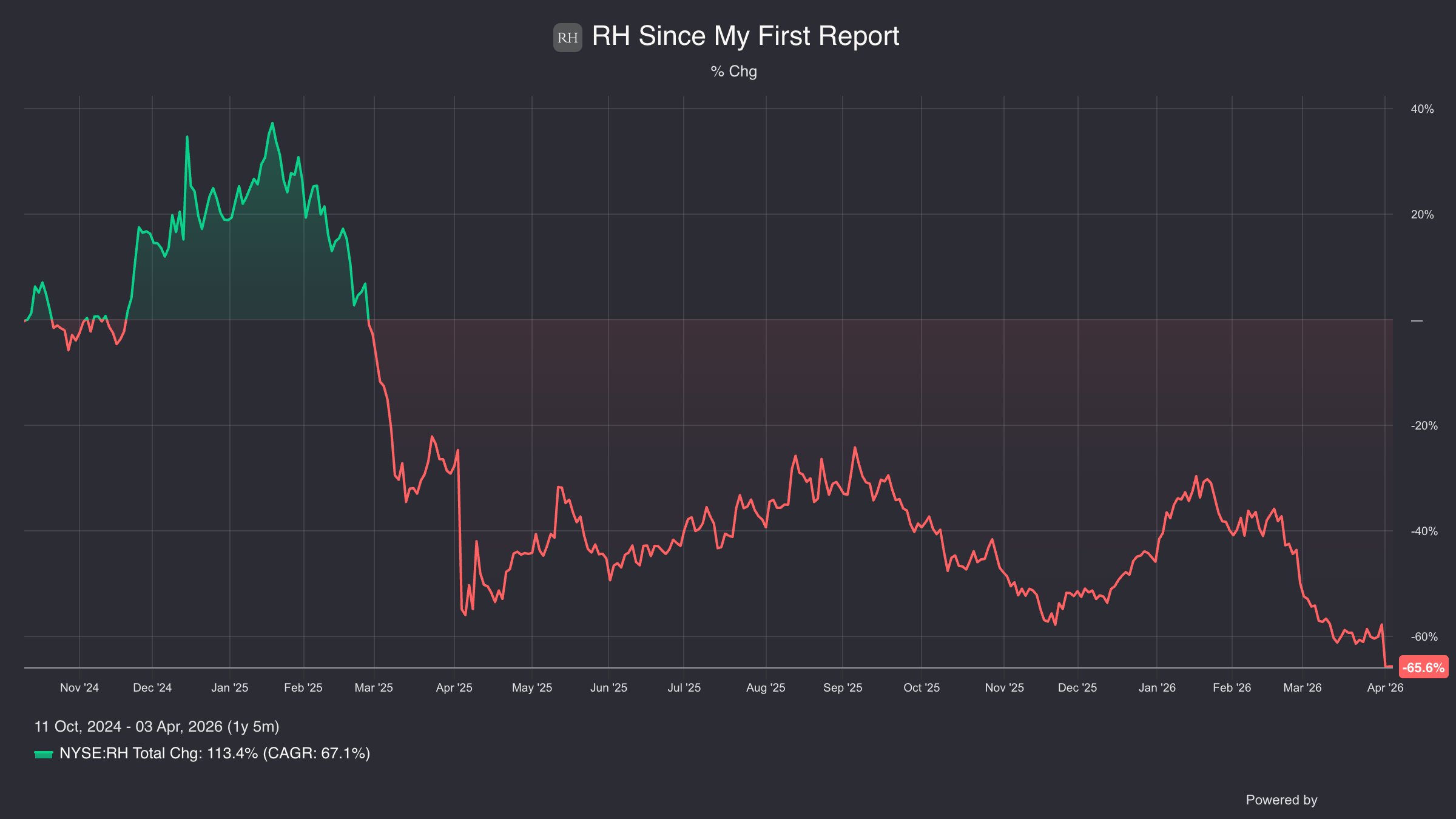

▶As you may have noticed, shares of RH RH 0.00%↑ have become frayed these days…

The last quarter and guidance continued to disappoint. While neither the struggling housing market nor tariffs helped, the reality is that the company appears to be struggling to the point of reaching. The proof is this comment from CEO Gary Friedman on the company’s most recent earnings call, when he said…

We’ve designed, I think, some of the most exciting retail concepts coming – it’s like new versions of RH that I think are mind-blowing, and they cost half as much. And we have other ones that are equally creative that will probably take less than half the time and cost less.

For quarters, these concepts have included “design compounds” and “design ecosystems” – all in the name of extending and expanding the brand faster.

But wait, you haven’t seen anything yet: In the most recent quarter, the focus turned to yet another new concept, RH Estates, which Friedman says “will become our largest and highest margin brand extension driving significant growth over the next several years.”

Running On Empty?

To my pal Rob Wilson of Tiburon Research, who also writes the Consumer EQ newsletter and probably knows more about RH since he once worked there as treasurer, the rollout of all these concepts “is a jump the shark moment.”

Or as he told me…

I think it says clearly that they’ve run out of opportunities to build these large stores with restaurants in the U.S. So, they need something to show that there’s still an opportunity for growth, and this is what they came up with. But, just last quarter, they were touting their “design studios” following the opening of the first one in Palm Desert. This was a 3,000-square-foot store that used to be a Lululemon store. Now they’re pivoting to focus on the ‘ecosystem’ stuff and they’ve not even opened one up… yet, are touting its potential.

He adds…

Beware any retailer touting something they’ve not yet tested. The rate of failure is high in those situations, in my experience.

Rob, whose client base is institutional – but also writes Consumer EQ – intends to elaborate on this in an upcoming report. (If you’re interested in retail investing, he should definitely be in your mix.)

Dream a Little Dream…

The thing is, it’s not as if he doesn’t admire what Friedman has built. “I want to be clear, what he’s done over the past 26 years is spectacular. I just question how big the business will become and how profitable it will be.“

And that’s the point: As I wrote in my original Red Flag Radar on RH, Friedman is an extraordinary marketer. He doesn’t know how to just sell the dream to consumers, but to investors as well.

Look no further than the latest narrative: Citing an estimated $30 trillion to $38 trillion “wealth transfer projected to take place over the next 10 years, which is more than double the past 10 years,” Friedman says…

Not only does the absolute dollar amount more than double, it's estimated that the dollars transfer from one to an average of seven people. It's possible over the next 10 years, our market will be multiple times larger than the past 10 years. When you combine that with our efforts to elevate and expand our product, globally expand our platform, generate significant revenues and brand awareness with our immersive hospitality venues, I would argue that the RH brand is in the perfect place, at the perfect time, and we will emerge from this period of clutter, discord and difficulty, as one of the highest-performing and most admired brands in the world.

To which Rob says…

When you put out pie-in-the-sky numbers for three to four years from now with very little detail about how the numbers may or may not look from here to there… and then, you come up with a thesis that says macro factors are the major driver (e.g., ultra high net worth individuals spend more on their homes and there’s a massive wealth transfer coming)… then, you’re done.

But it also keeps the dream alive…

Or as I originally quoted Rob as saying when the stock was flying, it feeds into the “irrational extrapolation” by analysts and investors who buy into Friedman’s thesis.

The difference between then and now is that reality is winning over irrational extrapolation. But as was the case then, RH remains a game of chicken… with the shorts likely to continue claiming their own victories along the way.

At least, that’s how it has been so far, with the stock rising nearly 40% in the months following my original RH Red Flag Radar, before… crashing, crashing, and crashing some more…

In the meantime, the dream lives on.

▶If you missed my report on AXT Inc. AXTI 0.00%↑, you can read it here…

Since then, the stock has been whipped around in what will surely go down as one of the wildest weeks for the market…

The stock took a major hit on Thursday on reports that Lumentum LITE 0.00%↑ was including indium phosphide substrates – AXT’s specialty – as part of a major expansion at a plant in North Carolina. I could not find any evidence of that, so I asked Lumentum’s IR, which responded…

I can confirm that we did not message any InP substrate manufacturing as a part of our manufacturing expansion in Greensboro. We did mention that this will be a 6”-capable fab for InP laser chip manufacturing, but our baseline plans for this site do not include the ingot-pulling, substrate manufacturing part of the process.

That, of course, doesn’t change the thesis of my report. Ultimately, as I wrote, AXT is a tale as old as the law of supply and demand. Doesn’t matter whether it’s high‑end optical networking gear during the dot-com boom, fracking sand during the fracking boom, or even pasture-raised eggs. Indium phosphide wafers will be no different.