Mini Case Study – AeroVironment Crashes

Drone maker falls from the sky as acquisition shows all signs of backfiring.

With the war in Iran, you would think that drone maker AeroVironment AVAV 0.00%↑ would be firing on all cylinders. Instead, it’s misfiring… and not in a small way.

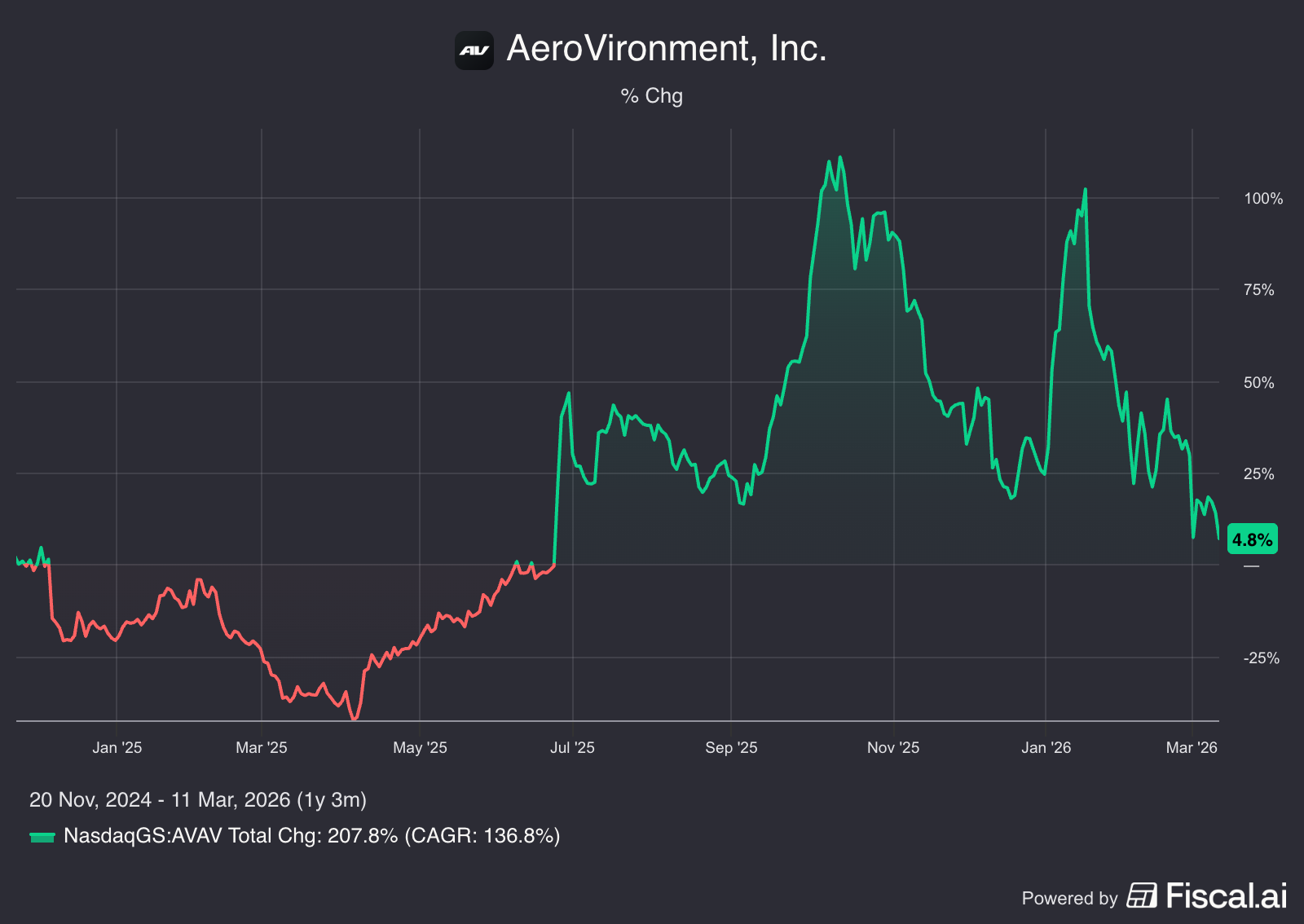

The reason it’s misfiring – highlighted by yesterday’s Q3 quarterly miss – appears to be the very reason I formally red-flagged AeroVironment in November 2024…. right before it took off like a rocket and doubled! (Never mind that it has since done two near-complete round trips, losing half its value over the last two months.)

At the time of my original report, AeroVironment had just announced it was spending $4.1 billion to acquire five-year-old BlueHalo from private equity. CEO Wahid Nawab claimed the deal would morph his company from being merely “the only profitable pure play unmanned systems companies publicly traded anywhere,” to “the leading pure-play mid-tier defense technology solution provider.”

This appears to be a deal out of weakness, not strength, in a story that boils down to this...

A sexy drone company whose growth is decelerating – but valued as if it’s still rocketing higher – is issuing new shares worth two-thirds its market value to acquire a non-drone, PE-owned company whose growth has gone into a nosedive.

Profitless Growth

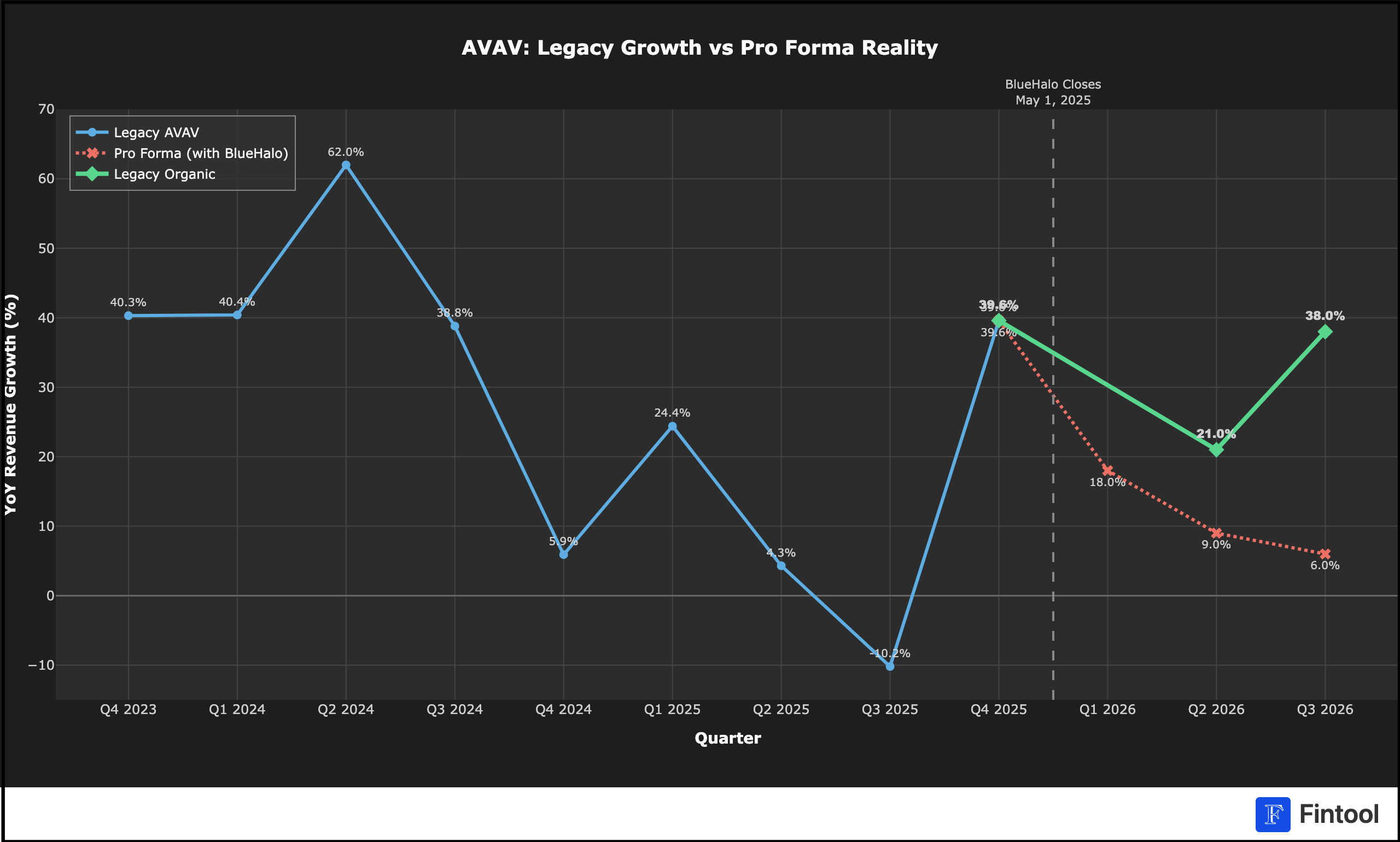

The irony is, AeroVironment’s legacy business is actually doing fine, but BlueHalo appears to have been nothing short of a disaster. If nothing else, this chart of legacy organic vs. its post-acquisition pro forma growth shows just how bad the deal has been…

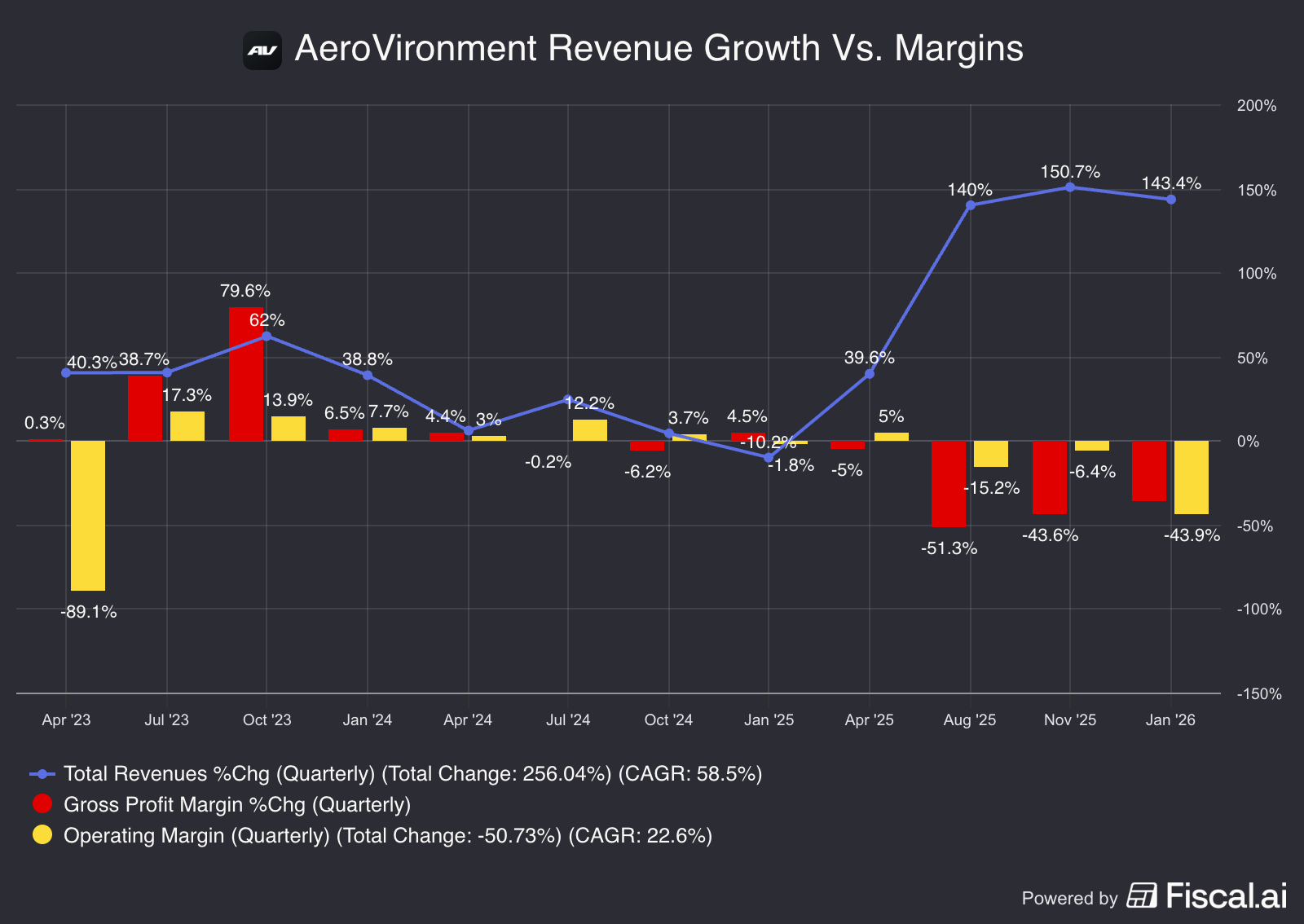

If you need more convincing, look at how a marginally profitable company became wildly unprofitable…

Now, AeroVironment is generating profitless growth, thanks to BlueHalo’s lower-margin services contracts and immature products that haven’t yet reached commercial scale. Or as CFO Kevin McDonnell put it on the earnings call…

“The business landscape of the combined new company has changed significantly with a higher service mix and several products in the early stage of maturation. “

Except, it hasn’t turned out that way… and management’s tone – triumphant three quarters ago – is now defiantly defensive.

In Their Own Words

After all, when the deal was announced in late 2024, Nawabi called it “transformational” and a “once in a generation opportunity.” Then, speaking at an investor conference last September, he said…

It's going to be a fantastic year with record revenues and profitability, nearly $2 billion in revenues and $300 million worth of adjusted EBITDA. We're going to be the poster child of what a defense tech company in the front should look like.

Then came yet another dose of reality, suggesting that if AeroVironment is the poster child of anything, it is on its way to becoming the poster child of what happens when a private equity seller is smarter than an eager corporate buyer…