The Wrap – Andrew Left's 'Bright Lines' Appeal

Also, Crypto, Bitcoin, Saylor's Strategy, G-III's tariff windfall. And for premium subs, updates on Modine, Signet, and Veeva.

▶A jury’s decision last week found activist trader Andrew Left guilty of securities fraud. I’m not going to rehash the case since plenty of others already have.

Instead, let’s hit pause and drill down to what really matters: The implications of Andrew’s promised appeal, which in all likelihood will lead to a landmark ruling.

As a journalist and researcher who has flown red flags for most of my professional career, I’ve spoken with, interviewed, and gotten to know more than a few of the most prominent current and former short-sellers. That includes Andrew, on-and-off, going back decades – well before his pre-Citron Research days – when he was known as Stock Lemon.

He was (and is) ready-made for the media: glibly eloquent and articulate to the point of being irrepressibly quotable… and doing so, most importantly: using his own name. On social media. In the press. And on TV, where he became a frequent guest. What made him different, and so appealing, was his willingness, mostly as a short-seller – with full attribution, no less – to talk trash about companies. It didn’t hurt that he had a good track record. That, in turn, gave him instant credibility in a world of anonymous stock scamsters, promoters, and even fraudulent social media bots.

Perfect Target

But that also made him the perfect target for eager populist prosecutors looking for low-hanging fruit – by focusing on the timing of some of his trades shortly after he promoted them. (Unlike Trevor Milton, who received a presidential pardon from prison after being found guilty of securities fraud and misleading investors at the late and not-so-great Nikola, now famous infamous for rolling a prototype truck down a hill to pretend it works. Or sell-side analysts who somehow find ways to justify stock targets considerably higher than their own discounted cash flow analysis. Or how about Strategy CEO Michael Saylor, who last year posted, “Sell a kidney if you must, but keep the Bitcoin.” He must still have two kidneys because earlier this week, Strategy … sold some Bitcoin? Cheap shot? Sure, but I digress…)

In a Tweet after the jury’s ruling, the U.S. Attorney who oversaw the case, Bill Essayli, said that Left had made “misleading statements to move the stock so that he could quickly trade on it for his gain. In essence, he cheated.” He went on to call that “fraud.”

No Bright Lines

But… is it? (Hint: By all accounts, given the vagueness of the laws about what constitutes fraud, it’s not.) Left says he plans to appeal. Win or lose, and regardless of what you may think of the merits of the appeal or the original case, or even the justice system, the decision could set a long-overdue precedent… drawing brighter lines for both longs and shorts between legitimate market influence and criminal manipulation. And perhaps more importantly, whether intent, timing, and the willingness to voice an opinion alone are enough to turn market commentary into fraud.

P.S.: If you missed them, two worthwhile reads on the topic: Edwin Dorsey of The Bear Cave, who spent two weeks in the courtroom. As a close friend and mentee of Andrew’s, Edwin writes about the trial from his perspective. And this post from longtime activist investor Carson Block of Muddy Waters Research, who makes it clear: Regardless of this ruling and all the headlines about how it will put a chill into what short-sellers say or publish publicly, he ain’t about to stop.

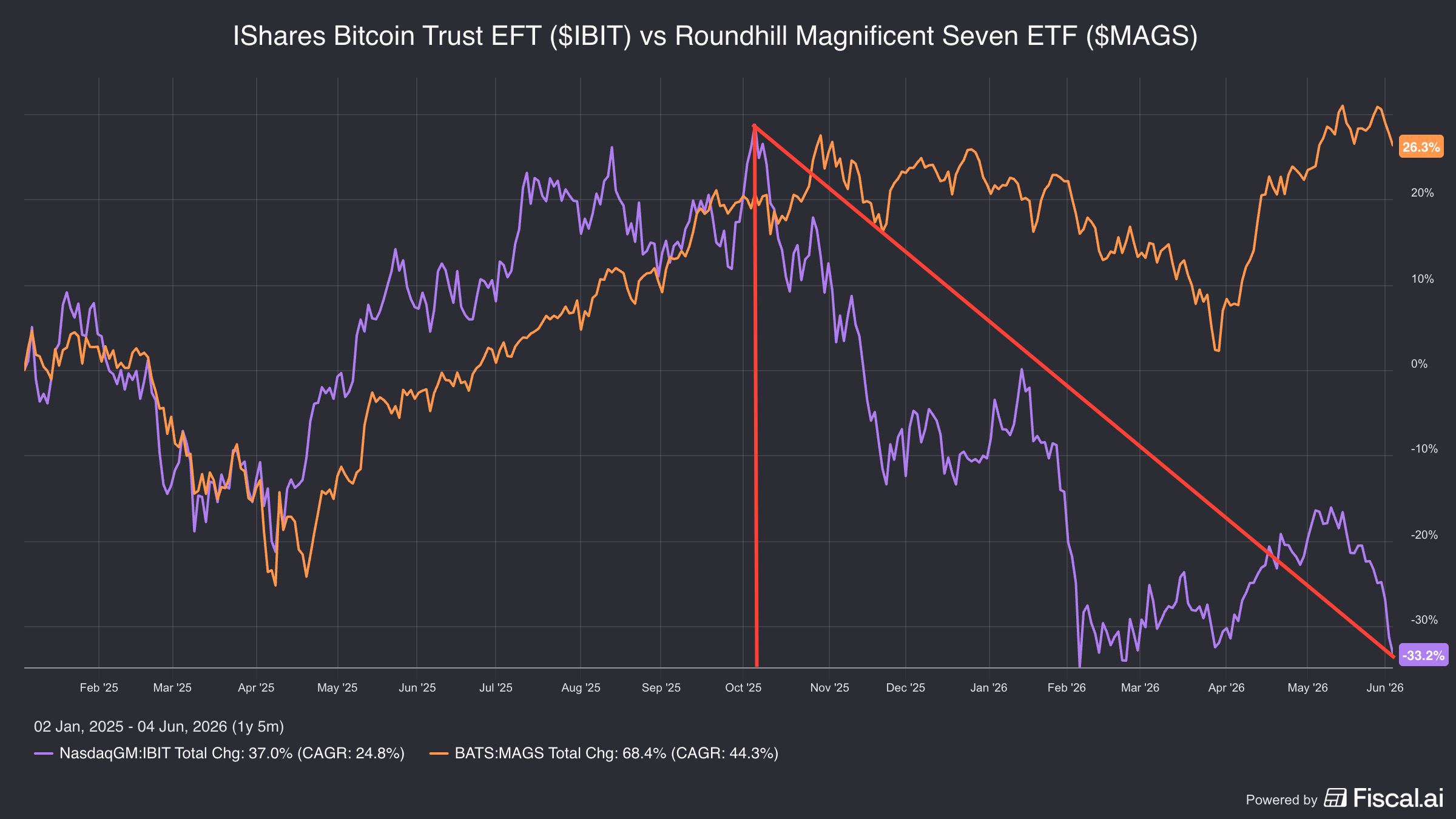

▶Meanwhile, back to the topic of Bitcoin… On Monday, exasperated that every time I turned around it seemed that AI had consumed the stock market – and pining for the old days of last year – I posted, “I’m old enough to remember when every other social media post was about crypto.” As the chart below shows, it wasn’t my imagination, starting last fall…

At the time of my post this week, Bitcoin was in the low-$70,000 range; it’s now more than $10,000, or 5%, lower.

There are all sorts of theories about what caused the Cryptonites to crater, but I favor the idea that SpaceX is akin to the Voldemort of IPOs, by sucking the life out of the room. The best explanation of that comes from Lawrence Fossi on Substack, who writes…

SpaceX is offering an unheard of 30% to retail investors, and they’ll have to come up with the cash from somewhere.

Thus, the IPO could cause major and disruptive selling — stocks and crypto are the two obvious candidates — by those raising cash to participate. Indeed, the downward pressure on $BTC in recent weeks might be partly attributable to such selling (with Michael Saylor recently adding fuel to the fire).

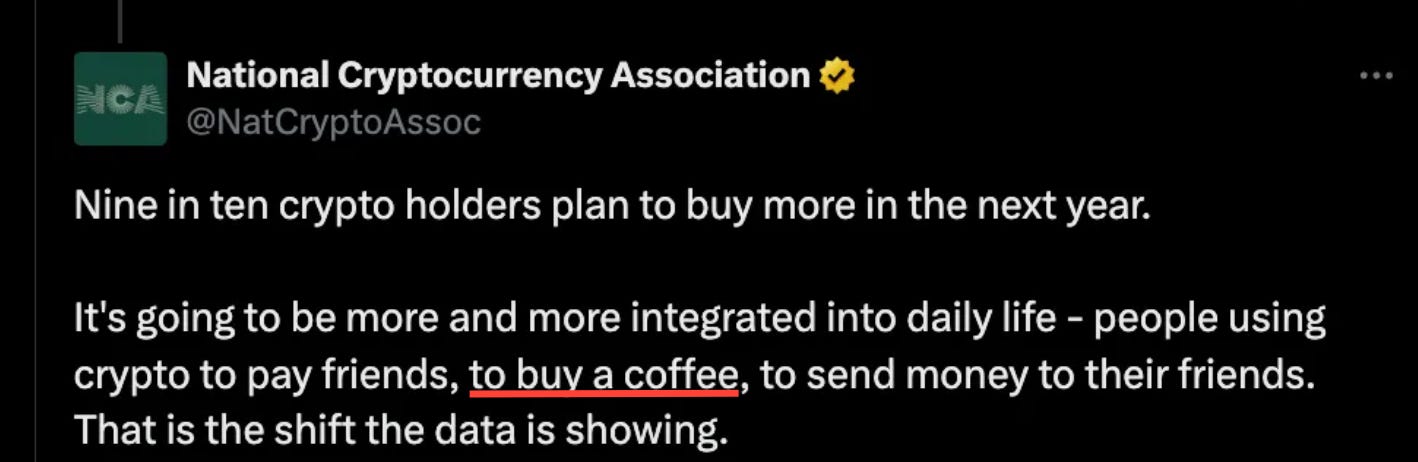

Yet another example of how humbling hubris can be. But beware, while the South may not rise again, the National Cryptocurrency Association responded to my post, suggesting that crypto will…

“Buy a coffee”? I take mine black. Onward…

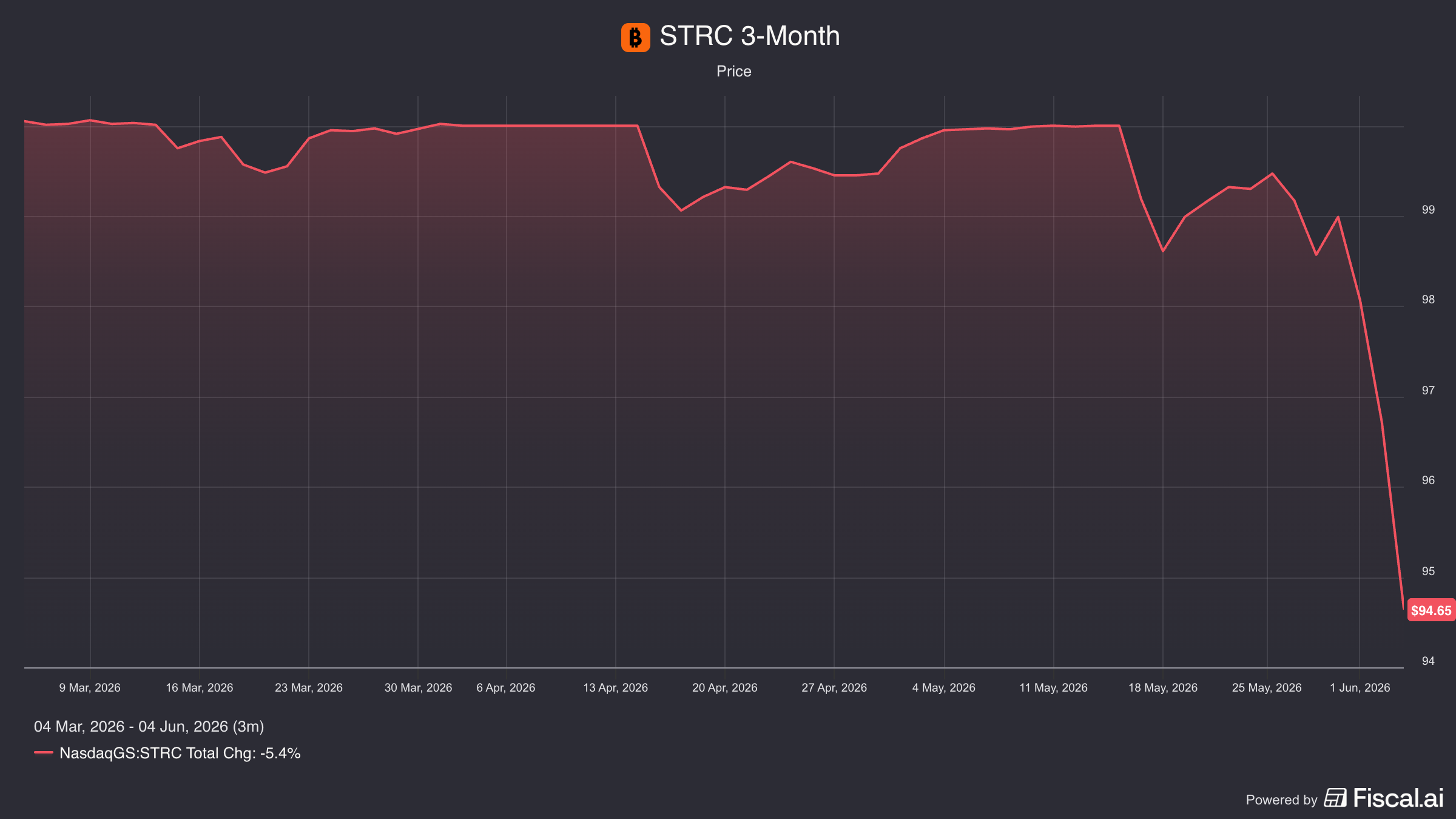

▶Speaking of Bitcoin, back to Saylor and Strategy’s sale of the precious faux commodity… The stated reason for Strategy’s sale of Bitcoin, Saylor implied, was to help fund the distribution of its STRC STRC 0.00%↑ preferred stock, which boasts a monthly dividend of 11.5%. To hear Saylor tell it, STRC is such a no-lose way to earn $11.5% that it’s good for conservative, income-oriented investors. I laid out that story in my “Michael Saylor, tl;dr: ‘Just Trust Me” from earlier this year, which you can read here…

Of course, burning the furniture to heat the house was never part of the plan… or shouldn’t be with an investment come-on for retirees, corporate treasurers, and the like. Neither was STRC selling below par, or $100, which it is now.

The beat goes on…

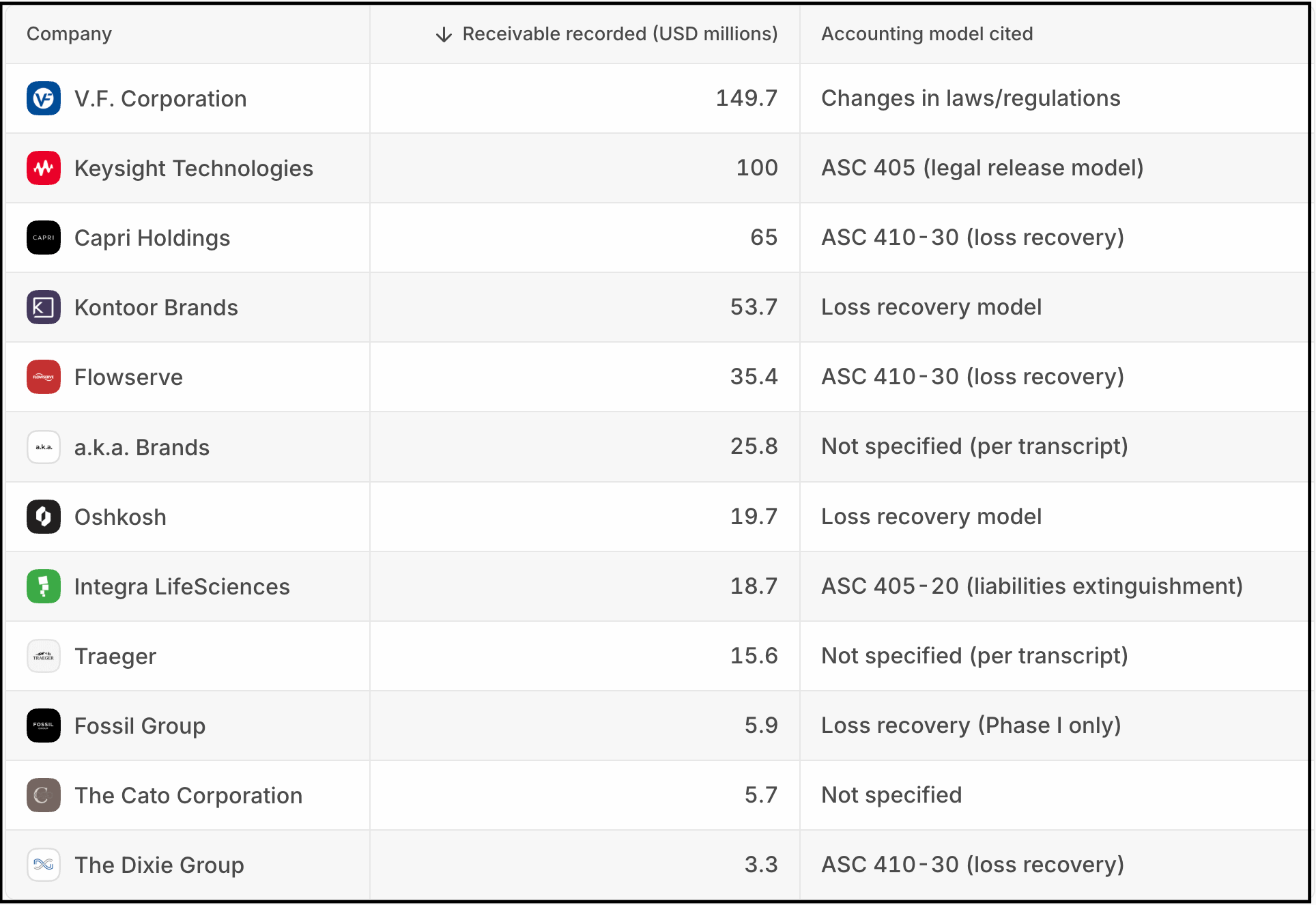

▶Turning to tariffs, if you haven’t noticed… A growing number of companies are recording non-cash gains on expected tariff recoveries. Just today, red-flagged G-III Apparel GIII 0.00%↑ did, helping lead to enormous outsized gross margins and net income. (And, in turn, its stock.) From its earnings release…

Gross margin increased 2,270 basis points to 64.9%, compared to 42.2% in the first quarter of last year.

Wowza, until you read the rest…

This increase includes a $102.7 million pre-tax benefit related to the expected recovery of previously incurred tariffs, imposed under the International Emergency Economic Powers Act (“IEEPA”) on inventory sold in the prior year. Excluding this benefit, adjusted gross margin increased 350 basis points to 45.7% from 42.2%.

G-III is hardly alone. With the help of Quartr, I identified a dozen companies that have done the same…

But not all companies agree, most famously and surprisingly, perhaps: the normally aggressive Tesla TSLA 0.00%↑. But there are others, like Adtran ADTN 0.00%↑, which said…

While the Supreme Court ruling establishes a legal basis for recovery, material uncertainty remains regarding the administrative process required to obtain refunds... Given the lack of clarity surrounding refund execution to determine expected recovery amount, the Company has concluded that recovery of the IEEPA tariffs is not probable as of the reporting date.

That, of course, is the conservative approach, which suggests earnings of those taking the aggressive approach, such as G-III, are relying on a one-time event to make things look better than they really are. As always, you have to wonder… why?

P.S.: I’m sure my pals Jeff Middleswart and Bill Whiteside at Behind the Numbers have been (or will be) having a field day with this. For a more technical view, Olga Usvyatsky of the all-things-deep-accounting Deep Quarry, took a look.

Updates on Modine, Signet, Veeva

▶In last week’s Wrap, I chatted briefly about how Modine Manufacturing MOD 0.00%↑had goosed its stock with what it called a “landmark $4 billion long-term capacity agreement.” The press release announcing the deal was heavy on hype and light on detail, to the point that there wasn’t even an 8-K filing, which usually accompanies material announcements. At the time, I hadn’t looked at the 10-K (shame on me), but buried among new risk factors in the filing was the most important of all details, which the company didn’t dare put in the press release…