The Wrap – Fraud, Grift... Does It Matter?

Also, IPO insanity and quick updates on Erie, Deckers

▶If you missed my squib earlier this week on the SEC’s proposals to “make IPOs great again” by lowering disclosure, along with a few other head-shakers, you can read it here…

In response, Olga Usvyatsky, who specializes in forensically digging deep through filings in her Deep Quarry newsletter, responded…

I have mixed feelings about that. Do we really believe that fresh IPOs have effective controls? And if not, is there a value in the attestation report beyond confirming that controls are ineffective or, in some cases, give investors a feeling of false security?

I responded…

As always, you ask a great question, Olga.

To me, it’s the simple issue: Less disclosure is not good for investors, most of whom these days couldn’t care less. Plus, EVERY company, it seems, is tagged for internal control issues. But with a less effective SEC and fewer disclosures, it would appear you’re setting the stage for less ethical management to seize the moment for their own good, with less oversight.

On the other hand, if passed as proposed, it will unblock the logjam in private equity, while at the same time lowering the overall cost and regulatory burden of being public… which may have swung to an extreme.

Now we’re swinging the other way, but mark my words: We’ll swing back, maybe to the middle, after the next “big one” because there WILL BE another big one, a-la Enron. People are people. Every generation throws a hero up the pop charts… fudging here, fudging there, thinking they’re smarter than they really are… and that nobody will notice, until they’re addicted.

And then they implode. And people point fingers. The politicians rush in. New regulators are embraced. Etc. Etc.

Wash. Rinse. Repeat. ;-)

▶I’m just opining from the far right field bleachers, of course, so let’s turn to my old friend Lise Buyer, who knows a thing or two about IPOs from being on the field. I first met Lise decades ago when she was a mutual fund tech analyst, then a sell-side tech analyst during the dot-com boom/bust, then at Google, where she was deeply involved in its IPO.

Here’s what she wrote on LinkedIn the other day, in response to the proposal (highlights by me)…

Great. Last time the regulators moved to "encourage" IPO activity, they did so via the JOBS Act, which, among other changes, eliminated the 500 shareholder rule. In doing so, they paved the way for private investors to exclude the public from the opportunity to invest when companies were, in general - there are always exceptions - in their most rapid phases of growth. The result? Unprecedented private market activity, the rise of massively funded, highly valued private companies, and a sharp decrease in the number of IPOs.

Now - the proposal above insures that potential IPO investors, those buying in as the early investors, look to harvest their rewards, have less information, delivered less frequently.Exactly who thinks adding incremental risk to the new issue market makes it more attractive? It may make it easier for issuers, but last I checked, markets need two sides. Skewing toward one side may be screwing the other...

Want more IPOs? Reinstate the 500 shareholder rule or an updated equivalent based on private round valuation. If a company has enough scale and enough shareholders, require it to file its financials publicly. There would be no IPO requirement, there never has been such a thing, but the obligation to share audited financials would both strengthen a company's internal financial muscles and be a catalyst toward a public listing - just as it was years ago for Google and (at the time) Facebook, among others.

There are ways to stimulate the IPO market for companies beyond the behemoths that may have drained the private wells. Less information for potential investors is not one of them.

Unless, of course, you're a grifter… or, worse, a fraudster!

Fraud, grift… doesn’t really matter what you call it. The lines, at this point, are blurred.

▶Speaking of IPOs, not-so-sudden thought: With the surge in mega IPOs while "the window is open," my mind harkens back to the oldest saying of all on Wall Street, which is as true now as it ever was: When the ducks are quacking, feed the ducks!

▶Meanwhile, for those keeping up with the Saga of Erie ERIE 0.00%↑ (Indemnity, that is)… the latest: On Thursday, CFO Julie Pelkowski will retire at year-end. She’s 56, which ironically is the same percentage decline of Erie’s stock since I first red-flagged it a few years ago. Her departure follows February’s announcement that CEO Tim NeCastro, 65, will leave… also at year-end. In between their departures, Chairman Tom Hagen departed. He’s the son of the company’s founder… and Hagen will be replaced by his son. Regardless, it’s a clean sweep… and it comes as competition only intensifies, with reported pricing per policy by the likes of Progressive PGR 0.00%↑ continuing to get more aggressive.

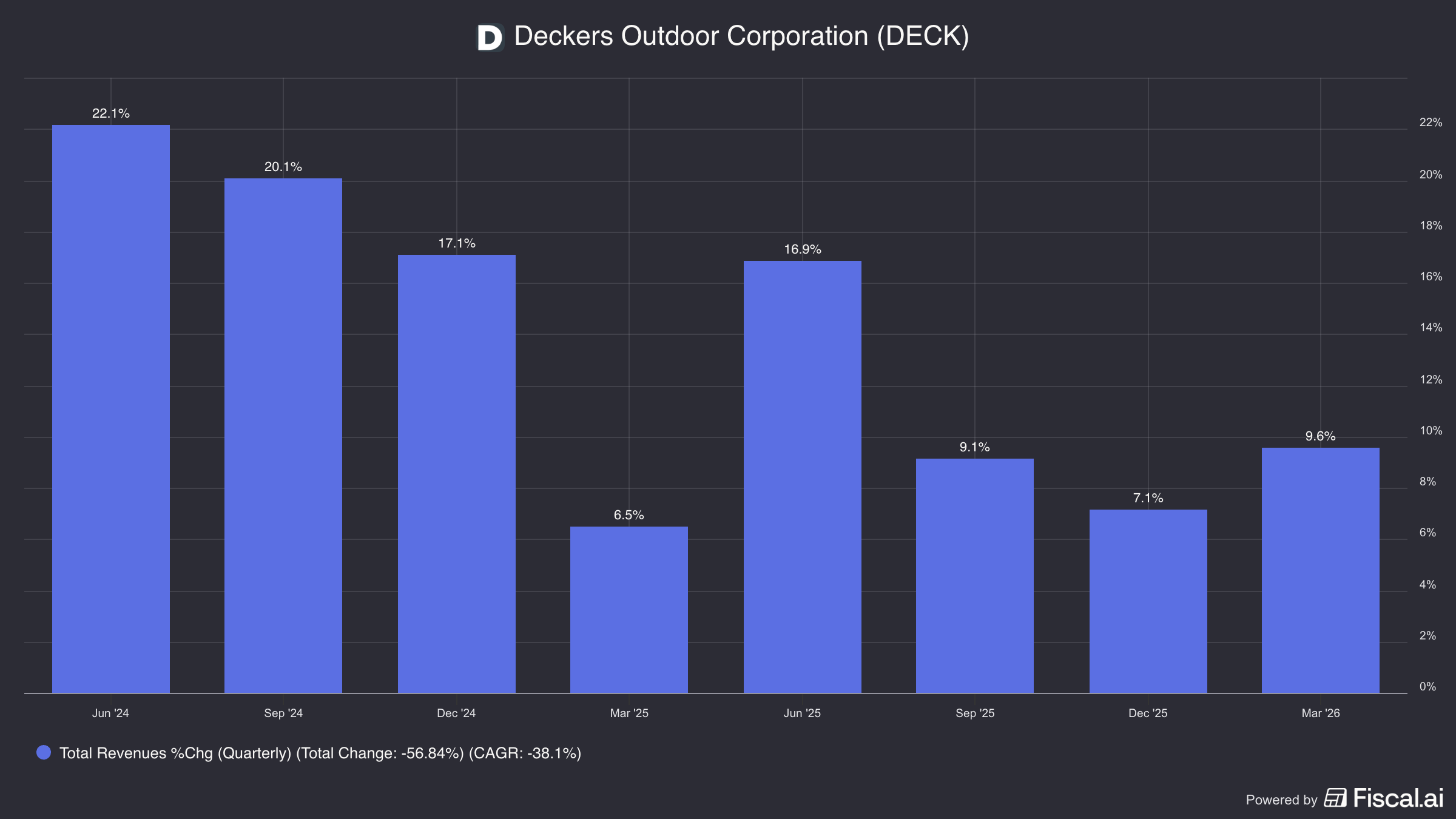

▶Finally, I first informally red-flagged Hoka/Uggs-maker Decker’s in June 2024, noting a subtle yet significant change in a single word in the company’s 10-Q, following up in February 2025 with a single added word. Since then, revenue growth has sharply decelerated…

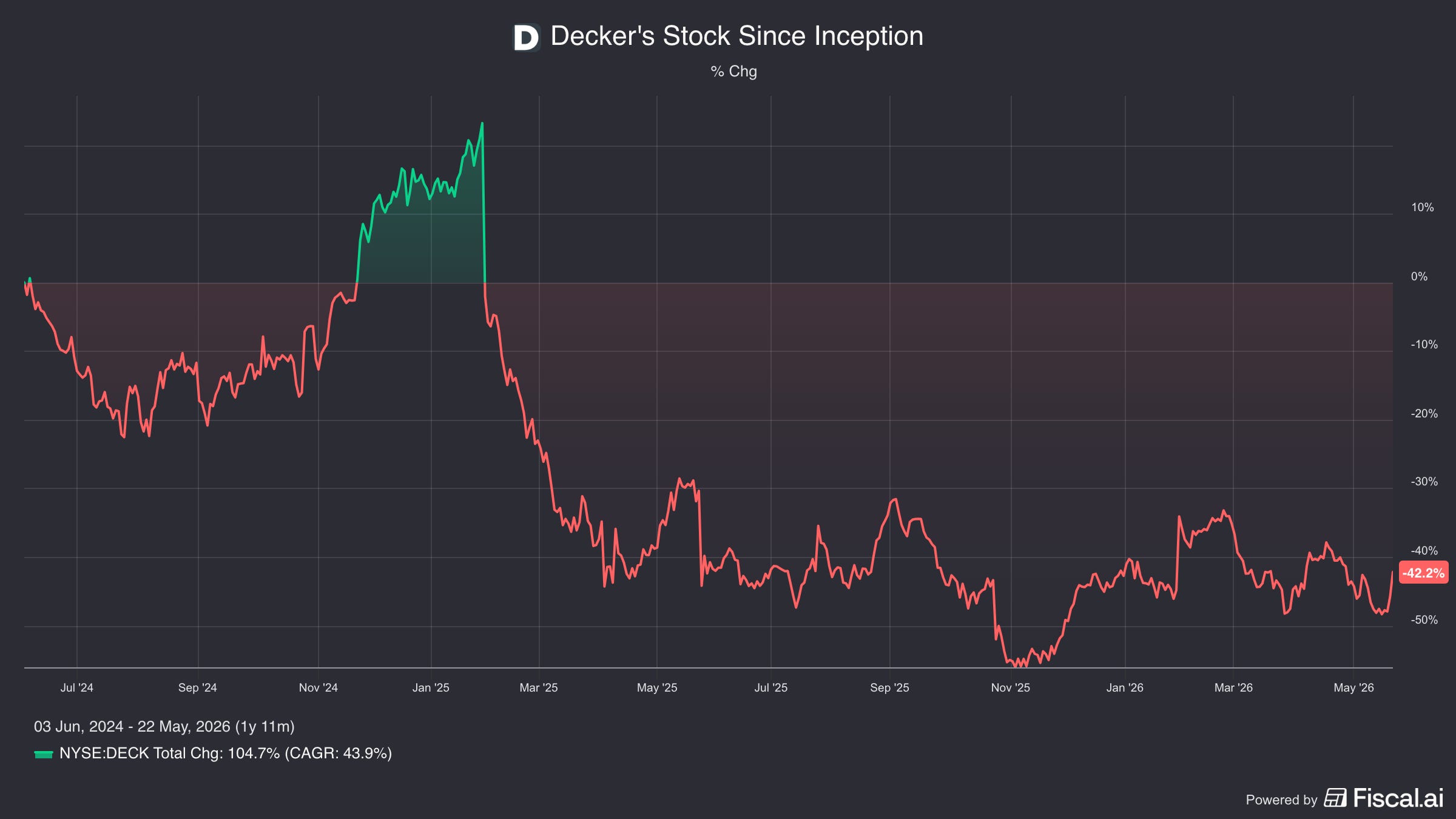

As has the stock price…

Yet, while there is no denying that Decker’s DECK 0.00%↑ did an exceptional job seizing the moment, culminating with the post-pandemic surge, management and analysts continue to promote a story that has decoupled from reality. Such as…