The Wrap – Tech Vs. Oil: Irrational Extrapolation?

Also, are data centers the next shale? Should we be nervous if the house is nervous? And... why are escrow agents so busy? So many questions, so few answers.

If you’re not currently a subscriber to my Red Flag Alerts, you can do so right here or get more info here.

Keeping it shorter/lighter than usual this week…

▶If you missed my report on why “Off the Radar” fave Roku ROKU 0.00%↑is selling to Fox and why now, here ‘tis…

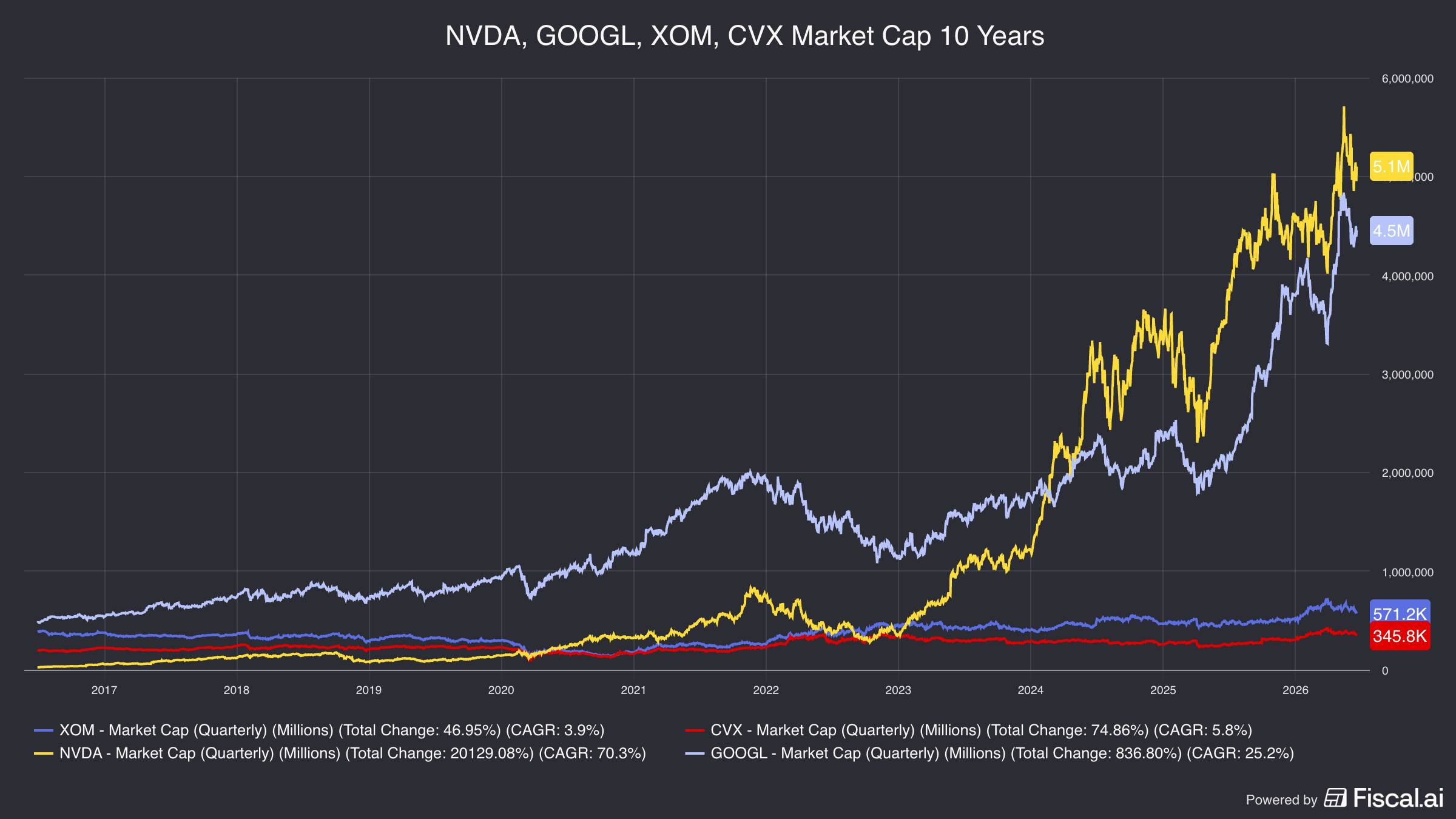

▶Tech vs energy: I meant to mention this one from my pals at Kailash Concepts weeks ago, but got sidetracked. This was a fantastic report drilling into the “extrapolation bias” that’s creating enormous valuation discrepancies between energy and tech. Their market caps tell that story…

The reason for such a wide spread: Tech has the highest percentage of companies reporting revenues above estimates. Energy is near the bottom. In other words – or so goes what would appear to be the natural extrapolation: Since it’s the only sector to have recorded a slide in its earnings growth since quarter’s end due to downward estimate revisions and negative earnings surprises, energy surely deserves its place in current stock market history.

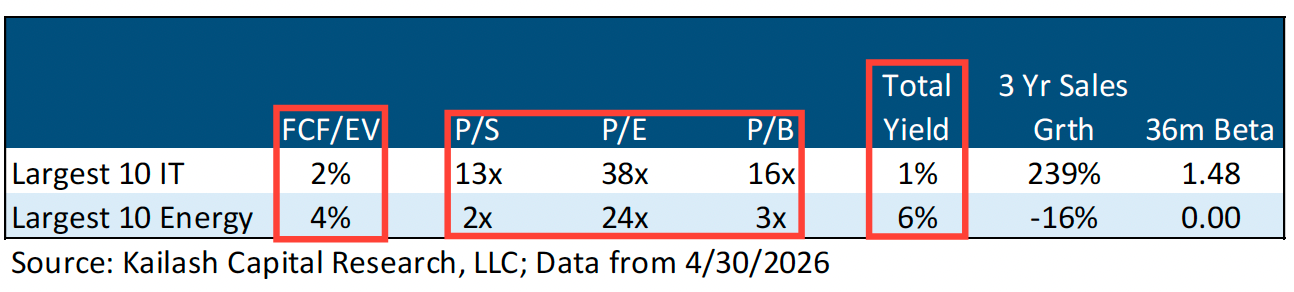

Sounds good on paper, but in KCR’s view: “Energy looks to us like NVDA and Technology did years ago; the bull case is in front of us, while analyst and investors’ bullish focus is fixated on Tech stocks due to their trailing performance,” best seen in the table below…

This is the classic perceived growth-versus-value-and-income conundrum. Or as KCR puts it…

Do you want to get paid 5% a year in total yield to own dirt-cheap energy stocks that are generating an 8% FCF Yield on $65 oil prices?

OR…

Would you rather own tech stocks that pay you nothing to own them and generate a nominal FCF Yield?

Or would you rather simply own SpaceX SPCX 0.00%↑? Everybody and every index fund on earth already does. And they all can’t be wrong. Or… can they?

▶Speaking of tech vs energy: Are data centers the new Shale? That’s the take of Harris Kupperman (Kuppy) of Praetorian Capital. In his latest, he writes…

This is a process. I don’t think we’re at the end of the buildout—not yet. These guys still have a lot of rope left to access cashflow, balance sheet capital and the equity markets. However, the pivot from buybacks to equity issuances is an intriguing signpost along the way. I think we’re finally at the point where investors start to get disgusted by the change in business plan. Then the re-rating starts.

Much like my oilmen, I suspect that the tech bros will just push ahead anyway, despite the pleas to stop. They’re chasing AGI, or creating a new god, or whatever it is that tech bros dream about—just like oilmen dream about drilling wells. It’s going to take a lot of pain to talk them out of this.

Hey, Kuppy, now do SpaceX.

▶Not what you see at a market bottom: Bloomberg reports that Charles Schwab SCHW 0.00%↑ is imposing new margin requirements for clients using long-short investment strategies that were once the exclusive domain of hedge funds. Or as Bloomberg explains…

The tighter rules apply to accounts using long-short investment strategies, in which clients borrow from Schwab to help finance portfolios that combine bets for and against stocks. The approach, increasingly popular among wealthy investors seeking to harvest tax losses while remaining invested, relies on a mix of margin loans and proceeds from short sales to finance those positions.

The kicker is that the only reason Schwab is doing this is that it “bears counterparty and balance-sheet risk if leveraged positions move sharply.”

When the house gets nervous, should we?

▶Finally, here’s a shocker: We just sold our house in San Diego so we can be closer to our grandkids in my old Bay Area stomping grounds. (If I miss a Wrap or two in the coming weeks, or there is a lag in new ideas, that’s why. Having moved 10-plus times, including a few coast-to-coast and back agains, I’m keenly aware of how much fun moving is not…and how disruptive it is.) But that’s the windup. The pitch: The escrow agent told us that she has never been busier. Who woulda thunk? As always, interpret at will.

If you liked what you read here, don’t be shy to click the heart… or to share this with your friends.

DISCLAIMER: This is solely my opinion based on my observations and interpretations of events, based on published facts and filings, and should not be construed as personal investment advice. (Because it isn’t!) I have no position in shares of any company published here.

I can be reached at herb@herbgreenberg.com.

I ramenber the shale oil comparison by Carlyle’s tech analyst you posted last yr. I see that dude on TV a lot now

You should get a medal for moving within CA rather than leaving. Did you ask the escrow agent where everyone is going?